Fission Uranium Corp.

COVID-19 Has Caused Uranium Supply Shutdowns and Fast-Rising Prices

This 25-Cent Company Has the World’s Next Round of Supply Already Confirmed to Be Worth $1.33 Billion

Fission Uranium trades on the Toronto Stock Exchange under the symbol FCU

& on the US-OTC market under the symbol FCUUF

Uranium is a hot topic these days.

The worldwide coronavirus outbreak has set in motion several catalysts that are kicking off a new uranium bull market.

The virus has caused several major production sources to come offline quickly and unexpectedly. And that has sent uranium spot prices to levels not seen since 2016.

Cameco, the world’s largest public uranium producer, has suspended production at Cigar Lake. That mine alone accounts for 13% of global primary mine supply on an annualized basis.

Now, Cameco has to buy the 1.3 million pounds that Cigar lake produces each month in the spot market, further exacerbating the situation.

What’s more, KazAtomProm in Kazakhstan, which supplies 40% of the world’s primary uranium, has announced a 3-month production curtailment. And that could be extended longer.

All this comes as many were already expecting a bull market in uranium based on pre-COVID fundamentals.

A US Dept. of Commerce Working Group was officially formed in July of last year to weigh US national security interests in light of America’s over-reliance on uranium imports from foreign sources such as Russia, Kazakhstan, and Uzbekistan.

The report is due out soon and could set the stage for even higher uranium prices going forward. Uranium spot prices are currently trading around $30 per pound with the market hoping to see something north of $40 per pound before too long.

![]() Against that broader backdrop, Fission Uranium Corp. (TSX: FCU)(OTC: FCUUF) is advancing one of the largest, highest-grade uranium assets in the world — the PLS (Patterson Lake South) Project, Saskatchewan, Canada.

Against that broader backdrop, Fission Uranium Corp. (TSX: FCU)(OTC: FCUUF) is advancing one of the largest, highest-grade uranium assets in the world — the PLS (Patterson Lake South) Project, Saskatchewan, Canada.

This project has scale: nearly 140 million pounds of uranium indicated plus inferred — one of the largest deposits in the world. It also has grade; 2% uranium which is about 10X the global average.

It’s also one of the shallowest uranium deposits in the world; just 50 meters below surface. There’s an old saying in mining, The farther down you go, the higher the risk! Hence, the exceptionally shallow depth of Fission’s PLS/Triple R Deposit goes a long way in derisking the project.

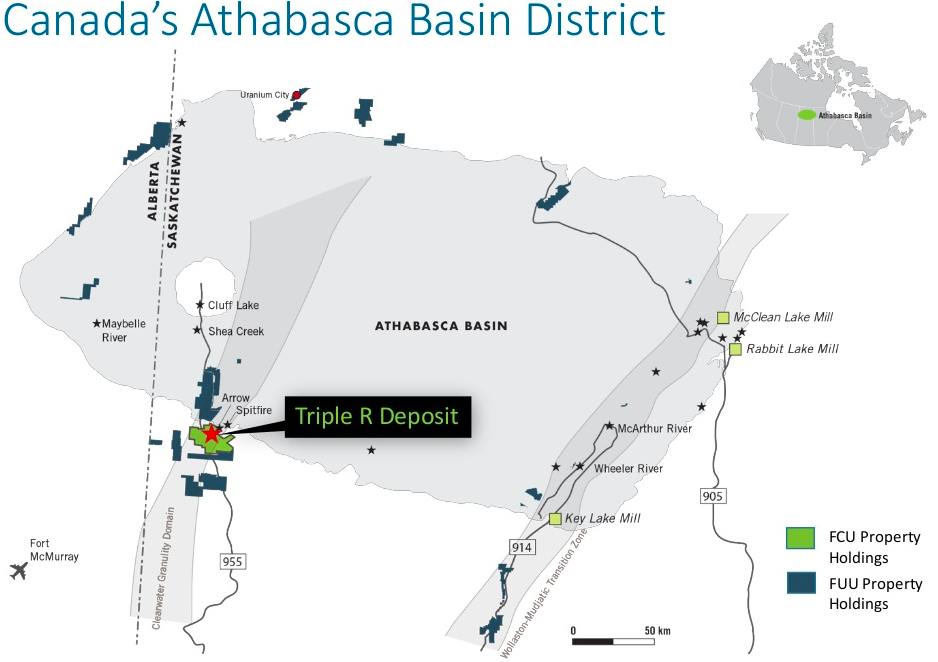

It’s also very strategically located just beyond the western edge of Saskatchewan’s Athabasca Basin — the world’s most prolific region for high-grade uranium.

A history of high-grade uranium discovery

If you follow the uranium sector, you already know that Canada’s Athabasca Basin lays host to the two largest, high-grade uranium deposits on the entire planet: Cameco’s Cigar Lake and McArthur River Mines.

What you may not know is that those two mines are well into their production lifecycles. TRANSLATION: The timing is impeccable for Fission Uranium which is aiming to commence production at PLS in 2025.

The macro environment is lining up nicely for Fission as well. The United States has a nearly 50 million pound annual uranium shortfall, of which about 25% is supplied by Canada.

Thus, it’s clear Fission is positioning itself to become an important future uranium supplier to the American market once all the hurdles are passed and its Triple R Mine comes online.

I’ve always said, “In the mining industry, you’re only as good as the people running the show!” To that end, I always prefer following mining professionals who have a history of making significant discoveries and then bringing those assets into production.

I’ve studied Fission Uranium extensively, and I’m very impressed with the company’s management team starting with Dev Randhawa, CEO, and Ross McElroy, president and chief geologist.

In a moment, I’ll be presenting you with my exclusive interview with Dev Randhawa. Dev’s expertise in the uranium mining sector is truly unmatched. In fact, I believe he’s now the longest serving CEO of any North American-based uranium company...period!

Ross McElroy is an award-winning mine-finder. He was an integral part of the Cameco team that discovered MacArthur River, the world's largest high-grade uranium deposit. In fact, Ross has been instrumental in 4 of the last 9 major uranium discoveries in the Athabasca Basin region including Fission’s flagship PLS discovery.

I’m impressed with this team, and I believe they have what it takes to get the job done for FCU/FCUUF shareholders.

It’s time to start looking at Fission Uranium

- PLS contains the Triple R Mine which includes 5 mineralized zones totalling approximately 140 million lbs U3O8 (indicated plus inferred)

- At 2% U3O8, PLS is considered one of the largest, highest-grade, near-surface uranium discoveries in the history of mining

- Fission has only scratched the surface of PLS with just 20% of the 120 sq mi property explored to-date

- New Pre-Feasibility Study confirms CAPEX reduction of $300 million and puts the asset into production one year earlier than previously indicated

- Projected OPEX of just $7.18/lb; IRR of 34%; NPV of $1.33B; potential to be among the lowest-cost sources of uranium in the world

- Ideal entry-point; Fission’s share-price is just now ratcheting above its 52-week low of C$0.09 per share

- READ BELOW: My exclusive interview with Fission CEO: DEV RANDHAWA

Fission Uranium is classified as an advanced-stage junior company now focusing on developing the PLS/Triple R Mine Project after making the initial discovery in 2012.

Many tangibles and intangibles separate Fission from its uranium development counterparts.

From a project perspective, the PLS deposit is located near surface at approximately 50 meters down.

This practically unheard-of proximity to surface significantly derisks the project, enabling Fission to develop a cost-effective underground mine plan that sheds about $300 million in CAPEX and gets the asset into production about a year quicker than previously projected.

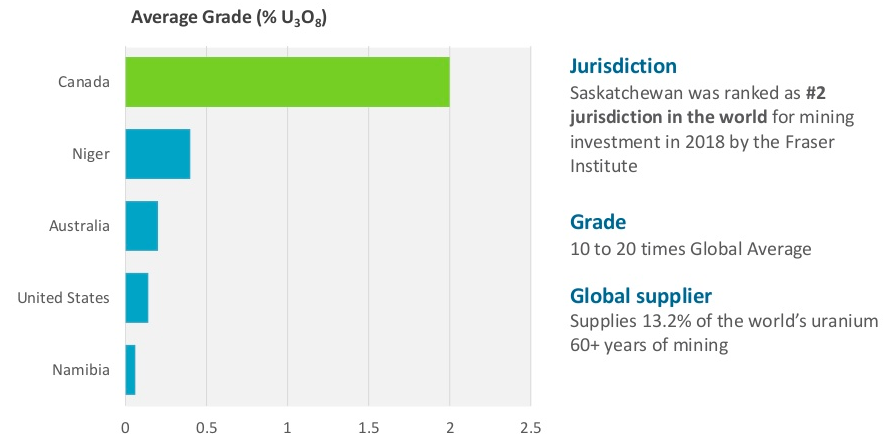

Another key tangible advantage is the richness of the PLS deposit. Global uranium grades average about 0.2% U3O8. Fission’s PLS project chimes in at around 2.0% U3O8 — a staggering 10X higher grade.

And remember this: Not just in real estate, but also in mining...location is key!

Fission’s PLS Project is situated in one of the most mining-friendly jurisdictions in the world — Saskatchewan, Canada. The Fraser Institute consistently ranks Saskatchewan in the top three jurisdictions globally with the province boasting a 60-year history of uranium extraction from the Athabasca Basin.

Additionally, Fission’s project area has roads, water, and existing infrastructure, all of which can go a long, long way in lowering overall development costs.

I could go on and on, including telling you how CGN’s C$82.2 million investment in Fission Uranium in 2015 marked the first time a Chinese company directly invested in a Canadian uranium company. But...why not hear it from the man himself?

Please enjoy my exclusive interview with Fission’s chairman & CEO, Dev Randhawa.

Exclusive Interview: Dev Randhawa

Mike Fagan: Dev, thank you for taking the time today. For investors who may not follow Fission Uranium, can you start with a brief overview of the company, the Athabasca Basin, and how your firm made the initial PLS/Triple R discovery?

Dev Randhawa: It’s my pleasure, Mike. As you know, Fission Uranium has just one asset. Yet, it’s a very large asset in Athabasca in the middle of Canada. The Athabasca region is well-known for its prolific high-grade uranium; it’s really the Saudi Arabia of uranium. Our property is located on the west side of the basin, and we made this discovery by thinking outside the box.

Pretty much every other mining company in the area at that time went looking for uranium on the east side of the basin. That’s where historically most of the uranium mines in the last 50 years have been located, and those deposits have mostly been unconformity deposits. You can think of these unconformity deposits like a milkshake sitting on top of hard rock. The unconformity is the boundary between those two geologic formations.

Our chief geologist decided to focus the team on exploring for high-grade uranium in the very under-explored western side of the Athabasca Basin, and, in fact, looking at basement rocks just outside of the current-day Athabasca Basin.

One of the tools we used effectively was a high-resolution airborne radiometric survey. That allowed us to prospect large areas of land effectively and quickly, in a matter of days, as opposed to ground prospecting with a large team taking months. By flying radiometrics, we were able to locate a high-grade uranium boulder field, and that’s how we started to make the discovery at PLS.

Our project technically isn’t even located within the basin itself; it’s a couple of miles out and is situated entirely in basement rock. And that means we don’t have an unconformity-style deposit, which has often been a challenge to mine.

MF: It definitely pays to think outside the box, Dev! So, the big news right now is that Fission Uranium just released an underground-only Pre-Feasibility Study for the PLS project. What are the key takeaways from that study, and is the company now settled on an underground-only operation or will there also be an open pit and/or ISL [in-situ leaching] component?

DR: The release of this study is a very important milestone for Fission. Our Triple R deposit is hosted in impermeable basement rocks and would be developed by conventional underground mining, or even possibly an open-pit / underground type. ISL requires the deposit to be situated in permeable sandstone. The Athabasca Basin has variable permeability, and ISL mining has never been attempted there, and so it’s an unproven method.

What our new Pre-Feasibility Study tells us is that compared to an open-pit, an underground-only operation can shave CAPEX by 20%, or $300 million.

The PFS also tells us that we can be in production a year ahead of schedule.

Open pit requires constructing a berm wall into Patterson Lake designed to keep the water out of the pit area. This berm wall has seasonality issues in relation to the construction period, and thus essentially adds an additional year to the construction time versus underground-only.

As you know, Mike, Saskatchewan gets extremely cold in the wintertime so certain things can only get accomplished during the warmer months. Really, the key advantages of going underground are economics, timing, and a smaller footprint when it’s all said and done. There are also advantages in terms of getting things permitted, obviously.

MF: PLS is a very large project. What’s the outlook, timewise, for payback from the initial CAPEX investment?

DR: As I mentioned, the underground-only option gives us 20% CAPEX savings, which is about $300 million. So instead of $1.5 billion, we’re looking at $1.2 billion to build out. This project may seem like a lot of money, but literally we’re looking at a payback period of just 2.2 years. That’s because the big heavy high-grade sits right at the top of the deposit. By mining this material first, we’ll be able to recoup our initial investment that much faster.

MF: That’s quick for such a large project...and you definitely have the right people at the controls to get things done. Tell me about Ross McElroy, Fission’s president, COO & chief geologist. I know Ross is very well regarded in mining circles, having won a number of prestigious awards for exploration and discovery with experience spanning both the major and junior mining sectors.

DR: Right. Ross was a part of the Cameco team that made the McArthur River uranium discovery – the world’s largest high-grade uranium discovery. He’s made two major discoveries for us; the Waterbury Lake uranium discovery and the PLS discovery. At last check, I believe he’s been instrumental in four of the last nine major discoveries in the Athabasca Basin. That’s pretty amazing when you think about it.

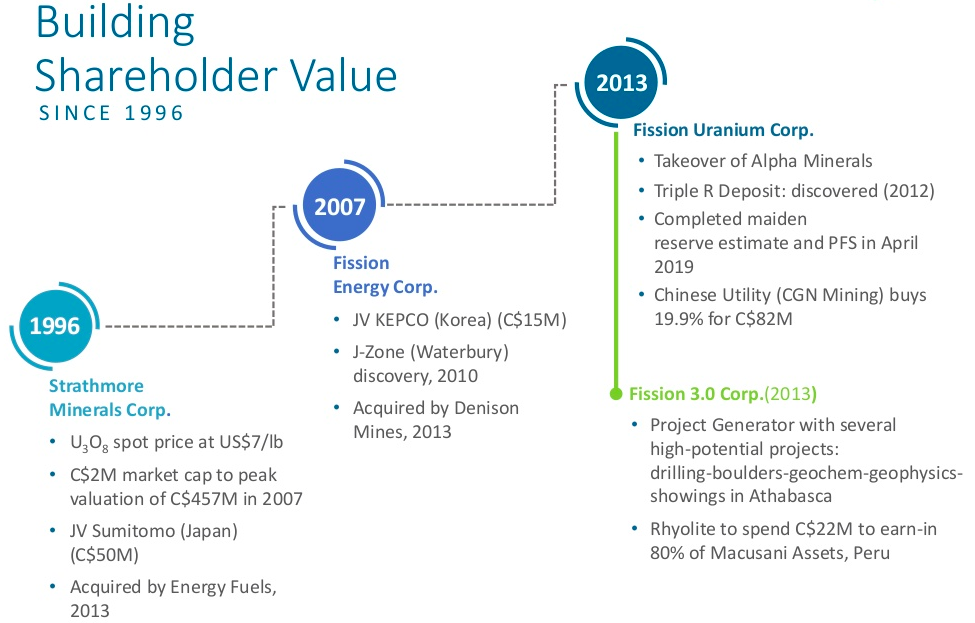

Ross is a very bright and very hard-working person who has built a really great team around him; we’re proud to have him. Our team is quite unique. We’re the only team in history in the uranium space that, if you owned a share of our first company, Strathmore, back in 2007, you can look at your account today and see that there are four active uranium companies in it.

We have a track record of bringing Asian money in. For example, when we started off as Strathmore, we brought in Sumitomo; that company eventually split into Canadian and US assets. The US assets were eventually sold to Energy Fuels, and the Canadian assets became Fission Energy.

We made a discovery with the help of a Korean utility who financed the exploration; we sold that project to Lucas Lundin and Denison Mines. We took the western side of the Athabasca and have now made two companies out of that. So, we’ve been very fortunate to have the right funding, the right technical team, and the ability to negotiate all of those deals with the Chinese government, the Korean government, Sumitomo, etc. We’ve been fortunate to have the right mix of talents on the job.

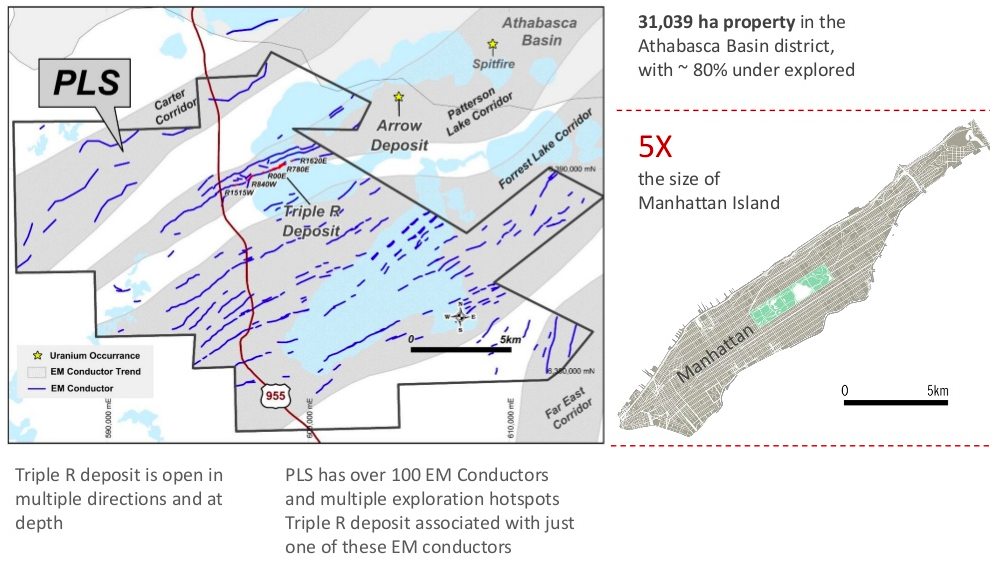

MF: Getting back to the PLS Project, you now have nearly 140 million pounds of near-surface uranium [indicated plus inferred] making it one of the largest, highest-grade undeveloped discoveries in history, and you’ve only drilled about twenty percent of the property. Can you share with me Fission’s outlook for additional exploration by way of the drill as we head towards 2020?

DR: Yes, the property is quite large…about five times the size of Manhattan. We haven’t done a lot of exploration over the last few years due to the uranium commodity price being too low. In fact, when we did make any kind of additional discovery on the property, we weren’t getting much upside from it in terms of our share price. So, we’ve really been focusing on getting the company headed toward production, which is prefeasibility, bankable feasibility, and filing for our licenses.

But you’re right, we’ve only really explored about 5% of the conductors. All uranium in the Athabasca Basin is found through conductors, but obviously not all conductors have uranium. We’ve only tested about 5% of these at PLS thus far, so there’s lots of potential for additional high-grade intercepts.

When uranium prices do turn around, and I fully expect they will, we should be able to raise additional capital and be more active on the exploration side of things. We could see an uptick in the uranium spot price as the 232 Petition gets resolved...hopefully later this month.

As you know, the US government has already kicked the petition down the road once. Right now, we’re watching things and it’s a fine line. In the uranium space, you need to balance not diluting yourself to death while also moving the project forward. So it’s a fine balance between the two.

MF: Your project sits next door to another top-tier uranium resource; NexGen’s Arrow Deposit. Many experts see this one-two-punch as the formation of a new Patterson Lake Mining District. Since a merger between Fission and NexGen does not appear to be in the cards, do you still see synergistic opportunities between the two firms such as the sharing of a mill and/or other infrastructure?

DR: I do. Obviously, when we develop our mine plans, we do so as individual companies. This is our property, that’s theirs...so to speak. Yet, it makes complete sense to have one mill and also to share a single airstrip. We’ve met with Leigh Curyer and the rest of the NexGen management team, and we certainly see the potential for sharing certain things down the road.

I firmly believe that the future of the Athabasca Basin is on the west side. Cigar Lake will be done producing uranium by 2028. McArthur River is the only one on the east side that’s practical after that. So really, the next pipeline projects are the PLS Project and NexGen’s Arrow Deposit, both of which are located in the west.

MF: Speaking of Cameco’s Cigar Lake Mine, resource investors will recall the catastrophic flooding that devastated that mine back in 2006. Fission’s PLS/Triple R Mine is also being constructed as an underground operation. What steps are being taken by your company’s mining engineers to ensure there’s not a repeat of Cigar Lake?

DR: Simply stated, Mike, it’s a completely different type of geologic formation. Cigar Lake is an unconformity uranium deposit where the ground conditions are quite problematic. Again, picture a milkshake sitting on top of hard rock. Where the two formations meet is where the uranium deposits are situated. That milkshake-type of setting causes rock stability problems and formational waterflow issues.

Fortunately for us on the west side and outside of the Athabasca Basin, we don’t have the unconformity setting nor the associated ground condition problems. There’s a bit of sandstone in the Arrow deposit, but nothing like what companies are dealing with on the eastern side. Remember, our deposit sits at just 50 meters below surface. Cigar Lake is 400 meters down. The deeper the deposit, generally the more mining risks to develop it.

MF: In terms of licensing, has Fission applied for a license with the CNSC [Canadian Nuclear Safety Commission] and the Saskatchewan authorities to operate the Triple R Mine, and how long is such an approval process expected to take?

DR: Yes, we’re starting the process with the CNSC this fall, and we are planning to submit what’s referred to as a Project Description. Overall, we could expect the entire Environmental Assessment period to take up to 2024, after which, if successfully dealt with, we could receive permits to build and operate.

MF: What about mine waste? This can oftentimes be a tricky regulatory endeavor to overcome, especially with an operation the size of what’s projected for the PLS Project. How does Fission intend to deal with tailings, and any regulatory concerns there?

DR: With the underground mining scenario, our waste rock is reduced by about 90% due primarily to the elimination of mining overburden. As for processed tailings, they’ll be deposited at on-surface tailings pits in our tailings management facility. That’s typically how it’s done for uranium projects in the basin, so straightforward from a regulatory perspective.

MF: Your largest investor, China-based CGN, has put over $80 million into the PLS Project with that funding coming in prior to the start of the US/China trade war. Any concerns as the trade war marches on?

DR: Politics are always difficult to predict, but the trade dispute is between the United States and China. Canada and China have had a pretty good relationship over the years. Canada has shown a strong willingness to encourage Chinese investment in the resource sector, so I don't see issues.

MF: You touched on Section 232 earlier. What’s your take on that?

DR: Well, as you know, in July of last year, President Trump declined to sign-off on the Section 232 Petition to the US Commerce Department, which calls for a Buy-American-Policy to reserve 25% of the domestic market [US nuclear utility demand] for US-mined uranium. Instead, a Department of Commerce Working Group has been formed to study the issue further. Not that governmental agencies have the best track record of being on time, but the anticipation is that they’ll be reporting their findings within the next couple of weeks.

Again, it’s hard to predict what governments will do. But I do know the study shows that the United States cannot, under any circumstances, provide enough uranium to fuel its 98 reactors. That means America will continue to require the bulk of its uranium from outside sources.

No matter the outcome, I feel confident that we’re in a good position as the US and Canada have always maintained a very close relationship. Fission Uranium plans on being a big part of that. Remember, the 232 Petition is really aimed at Kazakhstan. The petition doesn’t specifically call them out by name, but it’s implied that the US is receiving uranium from a country that’s partnered with an adversary; in this case, Russia.

Bottom line, it’s the uncertainty that’s causing most of the issues. We simply need the Working Group to release their findings and make their recommendations. Once that uncertainty is cleared up, I believe a foundation will be laid where uranium prices can begin to move higher, which will benefit both the United States and Canada.

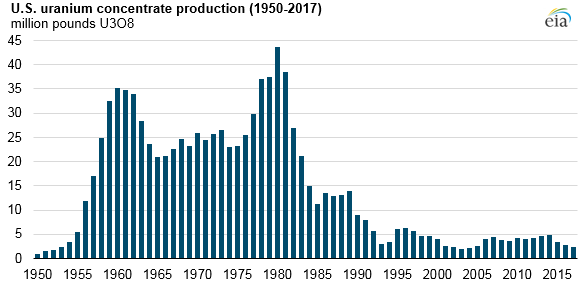

MF: You know it’s interesting because in the early 80’s America produced 40 million pounds of uranium a year when it only needed around 4 million. Today, the US requires about 50 million pounds and produces less than 2 million. Talk about that seachange and how it relates to uranium prices going forward.

DR: True. A few decades ago, there was a ton of investment in the development of North American uranium resources. The big oil companies were involved alongside the uranium-specific mining firms. The oil companies packed up and left, leaving the uranium space to a relatively small industry as commodity prices slipped.

To me, it all comes down to economics. As long as uranium prices stay where they are, the only companies that can truly make money are the ones with Canadian deposits because of the extraordinarily high grades.

Our uranium grades are running at 2% on average in Canada. US uranium deposits are more in the 0.1% to 0.2% range. So we’re talking 10X the grade. We also have a regulatory regime in Canada that understands uranium mining in Saskatchewan, so I think we’re in a good position going forward to produce at a profit.

MF: Speaking of high-grade, you could conceivably go into production at present uranium prices of around $30 per pound. Yet, I’m sure that’s not the internal rate of return you’re looking for. Ideally, where do uranium prices need to go for Fission to reap the kind of returns that are in-line with shareholder and company expectations?

DR: Sure, I firmly believe uranium prices will be much higher down the road. You have a cryptocurrency world that’s requiring more and more clean energy; in fact, they’re already using as much energy as the entire country of Switzerland. You have a long list of countries committing to nuclear energy led by China, Russia, and India. There’s also a lot of interest in small modular reactors like the ones Bill Gates is supporting.

The world needs clean energy and lots of it. I think as long as China wishes to replicate what America has accomplished, which is 20% of electricity coming from nuclear, then uranium prices in 2025 should be much closer to $50 to $60 per pound versus $30 to $30 per pound. The United States alone has this huge yearly deficit of nearly 50 million pounds, and there simply aren’t many companies that can produce at current prices. So uranium must go up.

From a production standpoint, we need $50 uranium, and I firmly believe we’ll get there. I see us going into production around the $50 to $60 range, which is where most pre-feasibility reports are done, because they’re assuming production in 2025, not 2019. But you’re correct, Mike, we could make money at $30 uranium, but it wouldn't be a lot of money at those prices.

MF: Dev, you’ve been in this business for a long, long time. In fact, I heard somewhere that you’re the longest serving CEO of any North American based uranium company (laughs!). I’m thrilled we had the chance to do this. Wrapping things up, what would you like to say to current and future Fission Uranium shareholders in terms of what milestones management is aiming to achieve over the next few business quarters?

DR: Mike, it’s been my pleasure. First, I empathize with these awful, awful spot prices and the impact it’s having and how much of the speculative money has left the space. What’s happening in the current uranium space simply does not make a lot of sense. We’re seeing a total disconnect between the uranium spot price and uranium-related stocks.

For example, our stock was trading at C$0.55 a share when uranium was at $18 a pound. Currently, uranium is up to $30 per pound, yet our stock has moved lower to around C$0.25 per share. So the speculative money has left the space; there’s no doubt about that.

Yet, as Rick Rule of Sprott USA often opines...you’ve got to invest in companies and assets where it’s a question of when, not if. So when this space moves, it moves quickly. We’re finally beginning to see that in the gold market. It’s the same thing I tell uranium stock investors, “Be patient.”

There are very few good names in the uranium space. We’ll survive this. We’re very fortunate to check every box that’s necessary for success. The Chinese government did not invest $82 million at C$0.85 a share with the idea for a trade. They’re invested in Fission Uranium for the long-term.

With regard to our PLS Project, they’ve selected what they see as the best uranium deposit in the world; it’s large, it’s high-grade, it’s in Saskatchewan, and it’s close to surface. There’s really no other uranium deposit like it.

I do like some of the other deposits in the basin, but they can’t touch the grade and shallow depth of our PLS deposit. It’s 50 meters below surface, and as we’ve shown, we can mine via open pit or underground. We’ll obviously lean towards underground as it enables us to get into production quicker and with less money. With our Pre-Feasibility Study completed, our focus will now shift to a Bankable Feasibility Study.

I understand it can be difficult to remain patient. I’m actually the largest retail investor in the space; I bought every share that I own. I was never given any at C$0.50 a share. I have 5 million shares, and I put my own money in. As an investor, you want to back people who’ve got skin in the game. And trust me, we have skin in the game.

Why Uranium, Why Now?

The Athabasca Basin region, which plays host to Fission’s PLS/Triple R Project, is known as the world’s leading source of high-grade uranium. This massive geologic formation is responsible for about 20% of the world’s uranium supply.

The United States is by far the world’s largest user of nuclear power with one-in-five American homes relying on nuclear generated power for electricity.

A full two-thirds of America’s clean energy consumption is coming from this source. In fact, nuclear is currently the world’s #1 source of clean energy…BIGGER than solar, wind, and all other renewable energy sources COMBINED.

Our planet will continue to require clean nuclear energy as a means of mitigating the global warming effects of greenhouse gas emissions from coal and other carbon-based fuels.

Yet, quite alarmingly, America is almost entirely dependent on foreign imports of uranium. That lies in stark contrast to the early-1980’s when our nation’s uranium was 100% Made-in-America. Today, with crucial trade barriers removed, less than 10% of our uranium is derived from American sources.

That’s all about to change...

America consumes a staggering 50 million pounds of uranium every year. Yet, it produces under 2 million pounds…less than what it brought to surface back in the mid-1950’s.

The US has 98 nuclear reactors…yet only produces enough fuel for one!

It should come as little surprise then, that in order to meet its robust demand, America imports a stunning 48 million pounds every year — making it over 90% reliant on foreign uranium sources.

And just WHO are some of America’s biggest suppliers?

Russia, of course, and its satellite states of Kazakhstan and Uzbekistan. In total, these nations supply around 40% of America’s U3O8 needs.

The risk to America’s national security is clear; drastic change is long overdue. That’s why the forthcoming recommendations from the US Department of Commerce Working Group in relation to the Section 232 Petition are so important.

Simply by removing the uncertainty surrounding the petition, we can expect US utilities to resume large-scale uranium market purchases, particularly as current term contracts with US producers draw to a close.

That should put some equilibrium back into the uranium market where spot prices can begin to move higher.

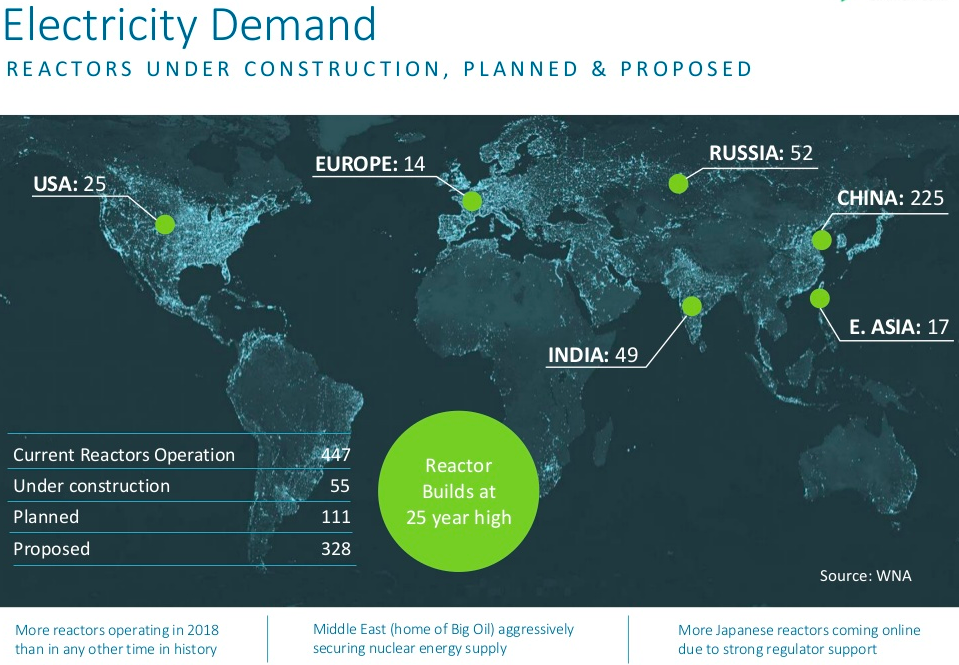

Demand for uranium will keep rising. Currently, there are 66 nuclear reactors under construction globally, most notably in China, India, and the UAE.

China has 45 nuclear reactors in operation, 15 being built now, and many more slated to commence construction soon. Saudi Arabia has agreements to build 16 new reactors by 2040. Thus, you can see demand growth coming from all corners of the globe.

While it’s difficult to predict with any kind of certainty exactly WHEN uranium prices will catch up to global demand growth...the bottom line is that it WILL happen.

When it does, companies with world-class assets in safe mining jurisdictions like Fission Uranium should be among the first to capture disproportionate gains in this beaten down sector.

Keep in mind also that Fission has only explored about 20% of the PLS land position. There’s tons of room for resource expansion by way of the drill, which could add precious pounds to an already large, high-grade uranium resource.

In Closing...

Today’s uranium market is showing very compelling supply-demand fundamentals over the mid to long-term that should lead to an upward trajectory in the spot price for uranium.

In my opinion, Fission’s PLS Project is one of the best PFS-backed, high-grade uranium deposits in the world. It checks every box – including size, grade, deposit-type, and jurisdiction – to become a successful producer down the road.

Fission clearly stands out as one of the most compelling opportunities in the entire resource sector for speculators with the right time horizon. The underground-only PFS revealed some positive numbers, and the company can now work toward a Bankable Feasibility Study.

I think the market will eventually wake up to the potential here...and any upward movement in the uranium spot price could prove to be a powerful catalyst for higher share values.

For investors who are interested in the uranium market, now is an opportune time to take a closer look at Fission Uranium Corp.

Fission Uranium Corp trades on the Toronto Stock Exchange under the symbol FCU & on the US-OTC market under the symbol FCUUF

Learn more about Fission Uranium and sign up to its investor list by clicking here.

And click here to get real-time updates from the company on their Twitter feed.

CLICK HERE FOR THE MOST RECENT INVESTOR PRESENTATION

Yours In Profits,

Mike Fagan, Editor

Resource Stock Digest