GoldMining Inc.

A Brilliant Growth Strategy

of Acquiring & Advancing Gold Projects in the Americas

— 25 Million Ounces in Gold Acquisition —

Set to Shine In a New Post-Crisis Gold Bull Market

TSX: GOLD — OTC: GLDLF

The GoldMining Inc. management team knows a thing or two about acquiring tens of millions of gold ounces on-the-cheap in safe mining jurisdictions throughout the Americas.

Following a decade of underinvestment in the gold industry – GoldMining Inc. has been able to systematically exploit the previous gold-market downturn by assembling an impressive portfolio of advanced projects encompassing 25.2 million ounces of gold across all categories.

The projects that comprise GoldMining’s resource were largely considered subeconomic when they were acquired between 2012 and 2016 at $1,100 - $1,300 per ounce gold.

Today, at $1,700 an ounce gold, these projects all of a sudden become much more interesting both from a production standpoint and as potential acquisition targets for larger producers seeking to add precious gold ounces to their balance sheets.

Poised for growth, GoldMining Inc. seized on a down-market for gold, built a sizeable asset base at low gold prices, and continues to do so as it closes on new acquisitions in 2020 that will further bolster its resource count.

Investor Snapshot: GoldMining Inc. (TSX: GOLD | OTC: GLDLF)

- Geographic diversification in safe mining jurisdictions; United States, Canada, Brazil, Peru, and Colombia

- Combined 25.2 million ounces of gold; measured & indicated (M&I) plus inferred

- Most acquisitions completed at $1,100 to $1,300/oz gold-price range

- M&I resources currently trading at approx. $15 per ounce in the ground

- C$8.6MM in Cash; No Debt; C$220MM market cap; C$1.50 share-price

- New acquisitions in 2019 and 2020 are set to add to the already impressive base of gold resources

- Creation of Gold Royalty Corporation led by David Garofalo and Ian Telfer. Shares to be spun out or IPOed

- New acquisitions in 2019 and 2020 have added to the already impressive base of gold resources

- READ BELOW: My exclusive interview with GoldMining Inc. founder & chairman: AMIR ADNANI

A Focus on Advanced-Stage Gold Projects

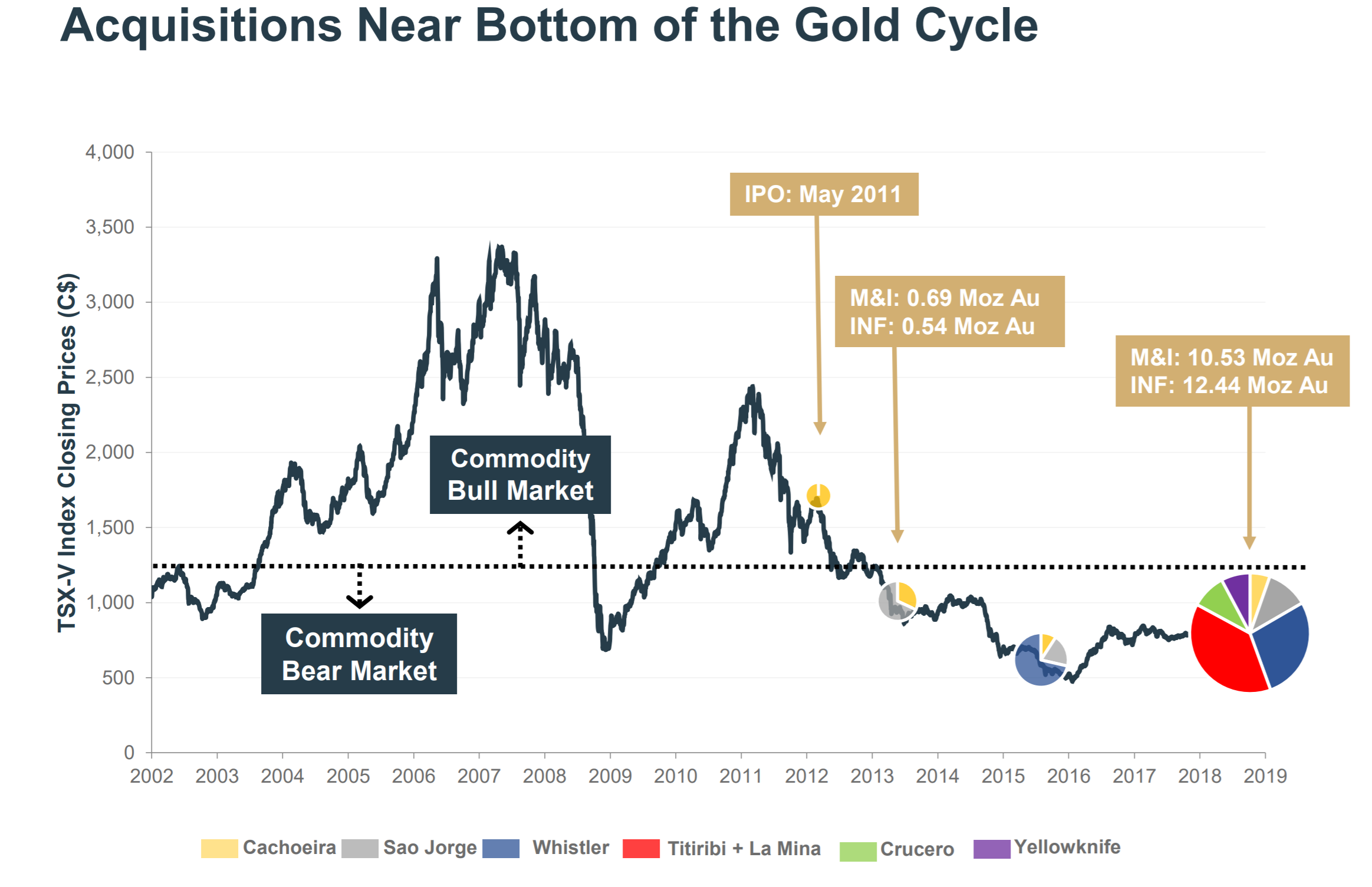

The gold landscape has changed dramatically since GoldMining Inc. completed its first acquisition in 2012. Back then, sentiment for the yellow metal was quite poor with gold languishing in the $1,100 - $1,300 per ounce range.

Today, that narrative has flipped with the yellow metal trading above $1,700 an ounce with indicators pointing to even higher gold prices going forward.

The Proper Acquisition Mindset

The GoldMining team was essentially put together for the stated purpose of exploiting gold’s temporary downturn knowing the cycle would eventually turn around to their favor… which it now has!

The team hit the ground running, scooping up no less than 11 advanced-stage gold projects in 5 countries throughout the Americas. Mind you, nine of the 11 were acquired during the 2012-16 gold slump at $1,100 to $1,300 gold.

When the dust settled, GoldMining had amassed a jaw-dropping 25.2 million-plus ounces of 43-101 gold resources — far more than any other junior resource company I can think of.

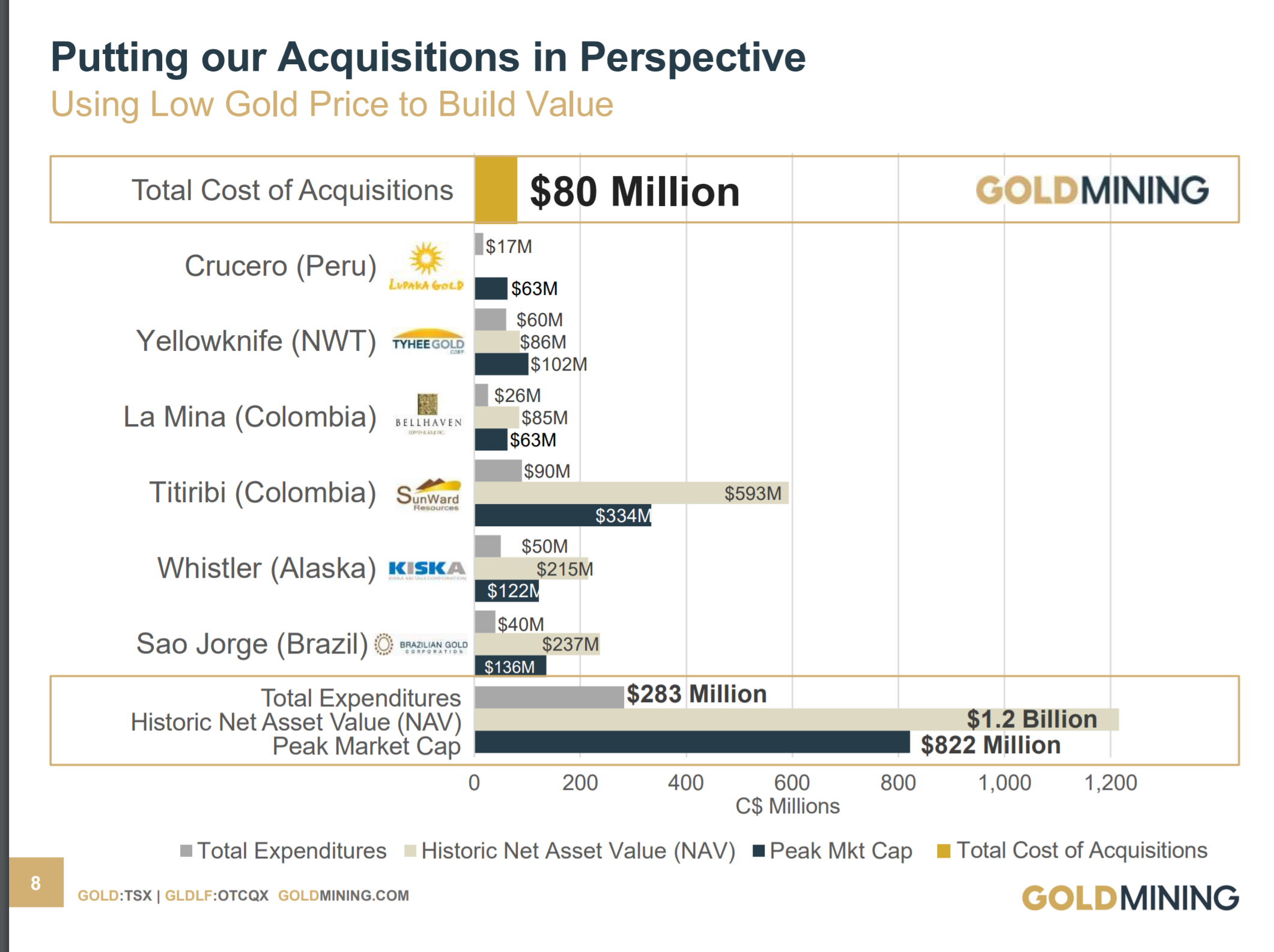

The chart below – showing the peak market caps of the companies GoldMining has brought into its portfolio thus far – tells the story well.

Combining for a peak market cap of C$822 million – GoldMining was able to pick up this entire group of exploration companies and their related projects for a grand total of just C$80 million!

That’s roughly 10 cents on the dollar!

Also revealing is the vast amount of prior exploration GoldMining has essentially inherited along with the projects. Cumulatively, these projects represent $283 million spent on prior exploration and drilling — resulting in substantial 43-101-compliant gold resources across the board.

The image (below) is yet another clear indicator of GoldMining’s unmatched gold-project acquisition acumen.

The first thing to note is the geographic diversification of GoldMining’s projects. That was management’s stated plan from the outset.

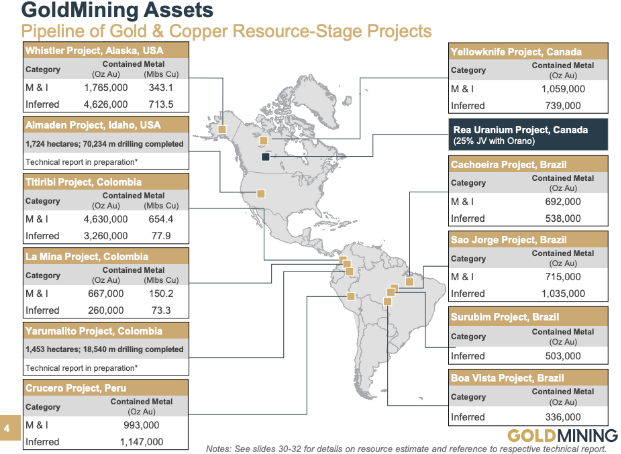

The company now holds advanced-stage gold projects in 5 mining-friendly countries: United States, Canada, Brazil, Peru, and Colombia.

The second thing is… HOW MUCH GOLD the company now controls.

GoldMining Inc. boasts a combined gold resource of 25.2 million ounces — 11.4 million ounces in the measured and indicated categories and an additional 13.8 million ounces in the inferred category — all spread across the Americas in safe mining jurisdictions.

The importance of jurisdiction cannot be overstated. It’s of paramount concern to both gold companies and resource stock speculators alike. That’s because the market typically applies a “political discount” to projects and companies operating in countries – such as China, Venezuela, Kenya et al – that lack in government-mandated protections for foreign mining investment.

Additionally, GoldMining has been highly successful in acquiring projects located in areas of large-scale regional activity. Again, this is all by design.

From the start, management has been astutely aware of the distinct advantages of working in active production zones where you have much larger companies — including intermediate and major producers — developing an area’s mineral reserves.

This is the type of environment where you typically witness large-scale area plays emerging along with heightened M&A activity. Its recent acquisitions in Colombia and Idaho are prime examples of this.

GoldMining Inc. now finds itself sitting on a combined 43-101 resource of 25,200,000 ounces of gold!

GoldMining is an extraordinary well-run company boasting a 9-year operating history of fiscal responsibility to shareholders, including:

- Well-capitalized with C$8.6M in the bank

- Advantageous price tag at C$1.50 per share

- ~C$220M market cap

- Strict focus on non-dilution of shareholders

And the gold is there!

GoldMining’s Titiribi Project alone boasts 4.6 million gold ounces measured & indicated plus another 3.2 million ounces inferred.

Add another 8 million ounces from GoldMining’s two North American projects (Whistler Project & Yellowknife Project) and you’re looking at 16 million total gold ounces from just 3 of the company’s flagship projects.

Think about it: It’s rare to see a pre-production company with even 5 million ounces of gold in the ground. GoldMining’s 20 million-plus ounces puts it in an entirely new ballpark.

When you factor in size, scale, and geographic diversification – it’s hard to imagine ANY mineral exploration company even coming close to equaling GoldMining’s acquisition success over the last several years.

That math is simple: In today’s climate of $1,700+ gold, it’s just no longer feasible to acquire that much gold at such little cost.

GoldMining’s 25.2 million ounces make the company highly leveraged to the price of the yellow metal, which should make for happy GOLD/GLDLF shareholders in today’s strengthening gold bull market.

And that total will soon grow again once the ounces from new acquisitions are formally factored in this year.

Exclusive Interview with Amir Adnani

GoldMining’s seasoned management team, led by founder and chairman Amir Adnani, has the company well-positioned for expansive growth. I had the opportunity recently to sit down with Amir. We delved into the gold mining industry as well as GoldMining’s strategy for building long-term value for its shareholders. I hope you’ll enjoy the conversation.

Mike Fagan: Amir, thank you for taking the time today. Based on your experience, what do you see as the main challenges facing today’s gold industry?

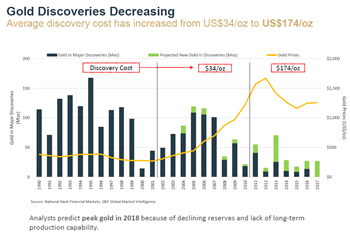

Amir Adnani: Pleasure to be with you, Mike. You know, one of the biggest challenges I’m seeing right now is that major gold deposits are becoming increasingly difficult to uncover. It’s interesting because you have industry insiders saying the sector isn’t spending sufficient cash to unearth new deposits. Yet, the reality is, since 2000, exploration budgets and spending have remained exorbitantly high despite the low number of significant new gold finds.

According to a National Bank 2018 report, average gold discovery costs have now increased from US$34/oz to around US$174/oz — a five-fold increase. Further, analysts are now predicting that peak gold was reached in 2018 as a result of declining reserves and a lack of long-term production capability.

Take for example moderate-sized gold discoveries of greater than 2 million ounces. The reality is that the sector is finding fewer and fewer of these types of deposits despite the steady rise in exploration budgets.

What’s more, the gold reserve life index of major producers has declined by an alarming 26% since 2012 and is now below key 2007 levels. That’s a major concern because sector growth is dependent on reserve increases across the gold industry as a whole. If the major operators aren’t panicking by now, they most certainly will be in the years to follow if the frequency of mid to large-scale discoveries continues to fall by the wayside.

MF: Some interesting dynamics at work there. With that said, did those macro factors have a degree of influence on how you went about setting up GoldMining’s growth-by-acquisition model?

AA: Absolutely. You can think of GoldMining’s business model as a consolidator/acquirer of advanced-stage resource-based projects. Our focus is and has always been on creating maximum value for our shareholders. Hence, the moment we recognized that bear market opportunity to build a large asset base at historically low gold prices — we jumped on it!

We completed our first gold-project acquisition in 2012 at the start of what proved to be an extended bear market for the yellow metal. During that span, as market fundamentals continued to deteriorate, we began acquiring additional projects in Brazil...then northward to Alaska...and so on.

Today, GoldMining Inc. holds advanced-stage gold projects in five mining-friendly jurisdictions across North and South America.

Remember, the majority of our acquisitions were considered sub-economic at the time of purchase as gold bounced around the $1,100 to $1,300 per ounce range.

Yet, what the market mistook as weakness was later proven to be a huge advantage for us as we were able to systematically acquire the entire suite of gold resource projects from all of these companies at about 10 cents on the dollar. The total combined peak market cap of the companies was C$822 million, and our total purchase was just over C$80 million — primarily in stock transactions.

MF: So you acquired, acquired, and acquired when gold was in the doghouse. Now, gold is up around $1,700 an ounce...which obviously is welcome news. And you’ve taken the very logical and well-received step of creating a royalty company — Gold Royalty Corp.. Why now?

AA: Why now is really an excellent question. First of all, when you consider that we've been at it for close to a decade acquiring resource-stage gold projects – again, most of it during the bear market period for gold – at some point, I think it was inevitable and we always felt that extracting a royalty from our portfolio would be another way to return value to shareholders.The timing now just seems, frankly ideal, for the simple reason that the market is really there, and is placing substantial premiums on royalty and streaming companies. And I'm not talking about just the established players that seemed to trade at premium valuations compared to the actual producers. On the emerging side of things, there must have been not a week that has gone by in the last few months where there wasn't a new royalty company announced.

So you look at that and you look at valuations that emerging royalty companies are getting on development-stage projects when they're requiring royalties, we just felt that this put us in a position where we can create this company now, Gold Royalty Corp. and be able to really give our existing shareholders this additional and distinct form of value enhancement. You look at the portfolio that we were able to start out with, it includes 14 newly created royalties as comprised of 2% net smelter return. Those are NSRs on two projects, 1% NSRs on 11 gold projects, and 1.5% NSR on one gold project.

The exposure is a lot of gold. As you know, we've got 11.4 million ounces of measured and indicated gold resources, 13.8 million ounces of inferred resources. Not only is it a substantial amount of critical mass with 14 royalties to come out of the gate with, but again, the exposure to this resource space that we've put together over the last decade and all the exploration upside, Gerardo. You look at the land that we cover. It's almost 1,300 square kilometers in 5 different countries.

All the elements that royalty and streaming investors like to have; exposure to the upside potential, immediate exposure to the underlying commodity, in this case gold, and the ability to have a diversified portfolio. All of those things that we have in place with GoldMining, you check all those boxes when you create Gold Royalty Corp. If you think about it, it is the right time to create this entity because you're able to pass that value onto GoldMining shareholders in a non-dilutive way.

Over the long term, obviously, we're going to explore the best value enhancing transaction for Gold Royalty Corp. Be it a potential spinoff, initial public offering, sale or merger, other transactions. But I can tell you myself, as the largest individual shareholder of GoldMining, we're going to do the most shareholder-friendly way. This initial step, obviously, it demonstrates that. We're not taking anything away from GoldMining shareholders. If you own shares in GoldMining, GoldMining owns currently 100% of Gold Royalty Corp. It's a wholly-owned entity and that value is very much there in place for GoldMining.

MF: Do you feel the jurisdictional diversification sets Gold Royalty Corp. apart from some of the newer royalty companies that we're seeing come in the space recently? You mentioned the abundance of royalty companies. I remember a time in 2016, and a few years prior to that, frankly, where prospect generators and project generators became the flavor of the month. Do you feel that having that diversity of jurisdiction sets the company apart and sets it up well, moving forward? AA: Absolutely. I would say, there's probably a few things here that we should really take note of. One is the fact that we've had a lot of interest and inquiries come in since the announcement. One question that's come up is, "Well, how come every other gold company doesn't do this? How come these other guys didn't do it?"The answer is, well, if you have one property or two, maybe three at max – your typical junior company will have a few projects that they're developing or focused on. Many of them, as you know, are single asset focused developers. What the royalty investor is willing to give premium valuation to is not only size, but diversification, that being in multiple jurisdictions.

So that's why the barrier to entry is high. You can't just be a single asset company or a single mine operator and necessarily do this. Absolutely, the fact that we have quite a bit of critical mass with the total resource space, but in addition to that the diversification, that sets you apart, number one.

Number two, many of the emerging royalty companies in the space right now, and even the big ones, by necessity have had to diversify away from gold. There perhaps is maybe 50% or 60% of their portfolio that is comprised of gold royalties. The rest is, in fact, everything and anything, ranging from oil and gas to other commodities. In this instance, you actually have 100% gold-only royalty with the 14 royalties that we've created newly.

The third point is, as you can appreciate, Gerardo, all the new players that are entering the space, they all have one thing in common. They all have raised a bunch of cash, and as royalty companies are capital providers, these new companies are looking to deploy capital to buy royalties. So, they're all trying to do the same thing and hence they're all competing with each other. It's hyper competitive. We didn't write a big check to have to acquire 14 newly created royalties.

That is what's so unique and rare here. In today's hyper competitive royalty landscape, where you see over $100 million dollars just get announced the other day by one of the biggest players. Wheaton Precious Metals, for example, just announced $138 million streaming transaction on the Marmato Project, which is in Central Colombia. In fact, just 12 kilometers south of the 3 projects we have in Central Colombia. When you see these giant checks be written, a company like Wheaton Precious can write a big $138 million check like that. But for the emerging players, that's a lot of money to deploy and you're competing with a lot of other players.

This is what really differentiates our story. We were able to just create 14 new royalties without writing a massive check. In fact, we didn't write a single check. As we move forward, this is another question that I've been getting, which is, "Well, are you guys not going to go compete with those other companies, those other royalty companies?" And the answer is, "No." We have a very distinct way that we can now and in the future grow and enhance our royalty business. As we do work on our existing portfolio of assets, that inherently increases the value of the newly created royalties that we have created and placed inside of Gold Royalty Corp.

Gerardo, as we make new acquisitions, and as you know, that's something we're good at. We've been doing that for a decade. We've acquired over $80 million worth of resource stage projects. That's how we have the portfolio that we have today. We will stick to our knitting, make acquisitions, and as we make an acquisition, we add that project to our total inventory so our mineral bank continues to grow, but then we create a new royalty on every new acquisition. That's how our Gold Royalty Portfolio can grow as well.

That is a very unique and different way than what every other royalty company out there is doing right now. Not only do you get 100% gold exposure, not only is it in a very diversified portfolio, but you're not trying to bring your checkbook to the party and compete with everyone else's checkbook on how to grow their royalty business.

This is in fact, though, for those that are familiar, what we're talking about doing, and this structure here is very much in fact how Franco-Nevada was created when it was wholly-owned by Newmont. Newmont was, as it was growing its business, placing these royalties into Franco-Nevada, and it was spun out. This is how Newmont, in a way, collaborated with Maverix and created Maverix. The new royalty company had a lot of royalties mended in by Newmont in that instance as well. You look at Wheaton Precious, it was spun out of Gold Corp in a very similar fashion.

Sometimes perhaps the advantage that a big property holder has, and in the case of GoldMining, you have that unusually large property for a company with our size and market cap. You cover the sector, you can confirm that. That gives you the opportunity, again, to be able to do what we've announced here, which is a non-dilutive layer of value to existing shareholders.

In a way, if you own shares in GoldMining, it's as though you're getting involved with the new creation of a new royalty company at the ground level. That is an exciting proposition in an environment where publicly listed royalty companies are trading at substantial premiums.

MF: No doubt about that. Plus you’ve got mining legends like David Garofalo of Goldcorp fame and Ian Telfer of Goldcorp and Wheaton Precious Metal fame to come run it.

So timing-wise, would you say now is a good time for investors to be looking at well-positioned juniors like GoldMining Inc. that are highly leveraged to the price of gold?

AA: Yeah, for sure. I view GoldMining Inc. as an excellent vehicle for resource investors to gain exposure to the gold market through ownership in a junior firm that holds a large asset base and is highly leveraged to the gold-price.

Each GoldMining share provides investors with exposure to a large and diversified gold resource portfolio of 25.2 million ounces [measured & indicated plus inferred]. Those gold ounces are distributed across 11 advanced-stage projects – all with substantial drilling and/or technical reports – within five pro-mining jurisdictions in the Americas.

These projects have been drilled out, thus requiring minimal cost for GoldMining to maintain. Needless to say, it’s quite the opposite of investing in a poorly funded junior explorer with a single, unproven and undrilled asset in a questionable mining jurisdiction.

We have a number of advanced-stage gold properties, significant ounces in the ground, C$8.6 million in the treasury, and sound geographic diversification. All of that serves to mitigate the underlying risk factors of investing in natural resource companies.

MF: Well said. Now, your company has always maintained a laser-like focus on advanced-stage gold project acquisitions. Can you tell me about your two most recent, done in late 2019 and early 2020?

AA: Both of these acquisitions really checked all the boxes in what we look for when we make an acquisition. You take the Almaden project, and this is a project in the state of Idaho. So what do we look for? We want to be in very specific regions where there’s mining, where there’s other projects being permitted and developed. And Idaho has definitely been a wonderful state and address to be in for development. Lots of other companies with bigger market caps than us, developing there, raising capital there, so we like it for that reason, number one. Number two, there was over 70,000 meters of diamond drilling done there. You just think about the replacement value of that would be well over $10 million and the time it takes to be able to complete drilling, et cetera. And we acquired this property for $1.2 million. Half in cash, half in stock.

So, we were able to structure a deal that really shows the market the types of transactions we are capable of doing, identifying, executing what we look for, and we certainly hope there’ll be a resource report coming out on this. That’s the next step and the next catalyst for us is to have a qualified person to complete a 43-101 resource report and put that out.

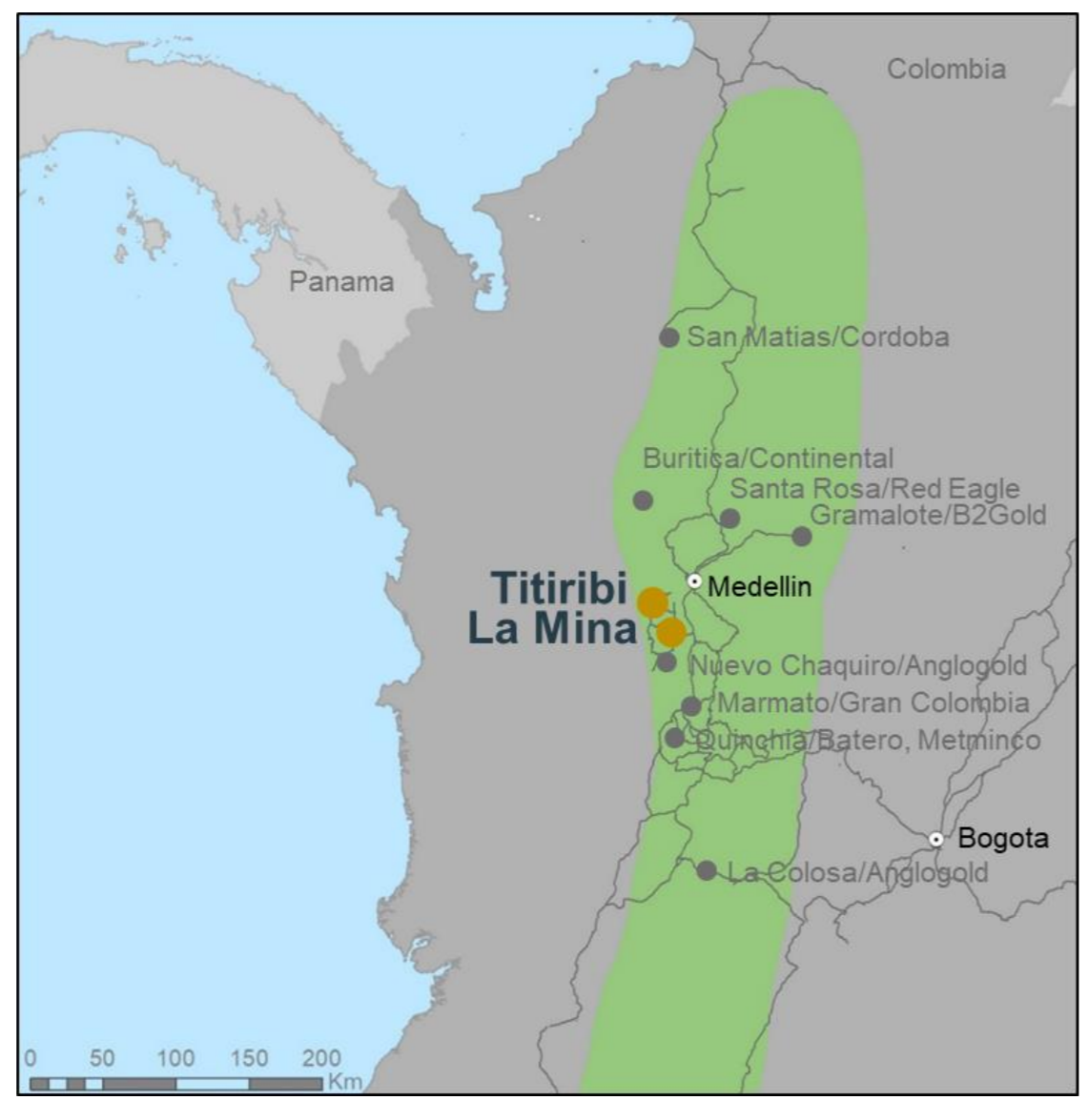

Same thing goes for the Yarumalito project in Colombia. We’ve been aggressively buying projects in Colombia’s mid-Cauca belt. Central Colombia, Nick, in the last 10 years they’ve discovered about 100 million ounces of gold here. It’s one of the least explored parts of the Andean belt in South America and Latin America. Major mining companies are very interested in central Colombia as evidenced by investments they’re making here, including recently Zildjian mining of China acquiring Canada’s Continental Gold for $1.4 billion cash.

That project is just 40 to 50 kilometers North of where we’ve made three acquisitions, including the very latest with Yarumalito. Again, another resource-stage project that we acquired for just over $1 million. Historic drilling, historic land acquisitions, all of which you’re buying for, honestly, less than it costs to even buy an apartment or condo unit in Vancouver and Toronto these days. I laugh about that because that’s the dislocation we look for in out-of-favor sectors where you can buy for a fraction of what the replacement value of the work is. So we’ve demonstrated that. Again, the next step is to come up with a resource report there as well.

If you think about our current valuation today divided by our existing total measured, indicated, and inferred resources, that valuation is one of the most attractive in the industry. But it’s going to get even more attractive as we increase our total resource space with the additional resources expected to come out in the weeks and months ahead of us.

MF: Speaking of the GoldMining Inc. valuation, I believe one of your South American properties, the Titiribi Project, had a peak market cap north of $330 million...or double the present market cap of GoldMining?

AA: Yes that’s true, Mike, and I’m glad you brought it up. As you know, GoldMining has a combined resource of approximately 25 million gold ounces across all categories. On top of that, we have a significant copper resource of approximately 2 billion pounds for a total global resource of 30 million ounces on a gold-equivalent basis.

Our Titiribi gold and copper porphyry project has an NI 43-101 resource of 6.22 million ounces gold equivalent in the measured & indicated categories plus an additional 3.44 million ounces gold equivalent in the inferred category. The property is located within the Mid-Cauca Belt, Colombia, one of the most prospective gold belts on the planet with over 100 million ounces of gold discovered over the last 20 years.

Mid-Cauca Belt, Colombia

One of the Richest Gold Belts in the World

At GoldMining, we’re interested in large-scale regional activity — that’s where the action is! This particular acquisition places us squarely in an area where billions of dollars are being allocated toward the development of metals deposits by the likes of Newmont, Agnico Eagle, IAMGOLD, and Gran Colombia.

We acquired the Titiribi project in September 2016 from the previous operator for a mere C$13.2 million in stock. Remember, this is an advanced-stage gold-copper project with excellent infrastructure and more than C$90 million spent on prior drilling.

We’re talking about a peak market cap acquisition of C$334 million – more than double the current market cap of GoldMining Inc. – for just C$13.2 million.

The following year, we acquired the La Mina gold project located less than four miles from our Titiribi property. Combined, these two porphyry projects bring our Colombian gold-copper portfolio to around 11 million ounces gold equivalent.

MF: Amir, as active market participants, we’re always looking for catalysts that can send the so-called generalist investors headlong into gold stocks — whether it be the majors, mid-tiers, or juniors. What catalysts, if any, are you seeing out there right now?

AA: Well, Mike, I always strive to look at things from multiple angles. You know, we’re seeing plenty of growth opportunities in today’s gold market. Yet at the same time, it’s important to be anticipatory of certain triggers that can drive even more generalist capital to the space.

One thing I’m always on the lookout for is consolidation within the majors and mid-tiers – and it’s been a banner year for that as you’re well aware. We just witnessed two of the biggest mergers ever in the gold sector: Barrick/Randgold and Newmont/GoldCorp. Those two deals are driving a ton of excitement to our sector, and it’s a trend I see continuing over the next few years.

As we touched upon earlier, we’ve seen a significant decline in gold production as a result of a full decade of underinvestment in exploration and development. During the most recent bear market for gold, the majors shunned growth-by-exploration in favor of deleveraging their balance sheets.

Today, with gold trending higher, you have a lot of companies that are cash flow positive, have solid balance sheets, and are poised for growth. That’s good for the overall health of our sector; growth starts with resources, and resources are the pipeline that leads to future mine development.

MF: True, it’s all about having significant resources in-hand when the market turns bullish...as it has now. In wrapping things up, Amir, can you speak to those same dynamics in terms of the junior space and GoldMining Inc. specifically?

AA: Sure, Mike. In terms of GoldMining...the nuts and bolts of it...we’re a junior gold company that successfully pieced together a very large resource at a time when gold was completely out of favor. By putting our collective noses to the grindstone, we were able to acquire over C$800 million in peak market cap companies/projects for just C$80 million. We now have over 24 million ounces of gold resources measured & indicated plus inferred.

As everyone knows, gold is now above $1,700 — so yeah, I really don’t see how our timing could have been any better.

I see GoldMining as being in a strong position for significant growth via accretive acquisition, the desrisking of our current projects, future M&A opportunities, and our leverage to the gold-price. At C$1.50 per share [C$220M market cap], I believe GoldMining offers an attractive enterprise valuation at $12/oz for a large diversified gold resource portfolio. Our company has C$8.6M cash on-hand and zero debt — and our share-price is up by more than 30% year-to-date.

In evaluating our portfolio, I think one thing investors recognize right away is how unique our resource is in both size and geographic diversification. I feel like the market is sleeping on us a bit right now. Yet, we’re not at all concerned about that. In fact, a snoozing market simply allows a window of opportunity to stay open that much longer for new potential investors to climb onboard.

By all accounts, the market is beginning to wake up to what 25.2 million ounces truly looks like in a rising gold market. Globally-renowned research analytics firm H.C. Wainwright & Co. recently confirmed its Buy rating on GoldMining Inc. with an updated price-target of C$7.00 per share. I think that says a lot about GoldMining’s near and long-term potential.

As we head towards 2020, I’m excited by the prospects of GoldMining Inc. attracting increased market attention as the current gold bull market continues to gain momentum.

MF: Amir, thank you again for the conversation...it’s been fascinating!

AA: My pleasure, Mike.

An Opportunity in GOLD

It’s hardly a coincidence that GoldMining Inc. trades under the symbol GOLD! The company has amassed a veritable treasure trove of the yellow metal and is now poised to move up substantially on any future rallies in the gold-price.

As you can see, gold is in the midst of a brand new bull market...rallying from $1,200 to $1,700+ an ounce in just the last 12 months.

The healthiest bull markets are ones that grind higher – not shoot straight up – and the above chart indeed shows that gold is grinding its way toward $2,000 an ounce...and perhaps much higher.

With gold flexing its muscles, it’s easy to see the value of owning shares in a company like GoldMining Inc., which is highly leveraged to the price of the yellow metal.

Analysts are beginning to take notice as well!

With 25.2 million gold ounces across all categories – along with the potential to add even more gold via acquisition – renowned research analytics firm H.C. Wainwright & Co. recently reiterated its Buy rating on GoldMining Inc. with a price-target of C$7.00 per share.

That’s more than 2000% higher than GoldMining’s current price of C$1.50 per share – and even that price may prove conservative if gold rallies above $2,000 an ounce as many top commodities experts, including analysts at Citi, are predicting.

A focus on value.

In the resource sector, you’re only as good as the people running the show – and I have every confidence that GoldMining Inc. has the right personnel at the controls to build value for GOLD/GLDLF shareholders going forward.

You heard from founder and chairman, Amir Adnani, himself. This is a man who, along with his team, knows how to get things done in the resource sector.

It’s a team that’s highly committed to building long-term value for its shareholders — and the proof is in the numbers. The company currently has C$8.6 million in the treasury and hasn’t needed to go to the markets to raise capital since 2016.

It’s that type of sound corporate governance that has allowed the company to amass an astounding 25.2 million gold ounces for mere pennies on the dollar.

For investors seeking exposure to a rising gold market — GoldMining Inc. holds tremendous upside from current price levels.

GoldMining Inc. trades on the Toronto Venture Exchange under the symbol GOLD and on the US OTC Bulletin Board Exchange under the symbol GLDLF.

Learn more about GoldMining Inc. and sign up to its investor list by clicking here.

And click here to get real-time updates from the company on their Twitter feed.

CLICK HERE FOR THE MOST RECENT INVESTOR PRESENTATION

Yours-In-Profits,

Mike Fagan

Editor, Resource Stock Digest