Revival Gold RVG.V

3 Million Ounces of Gold and Counting

RVG is Positioned-for-Gains in the NEW Gold Bull Market

Gold is soaring. The yellow metal recently broke above $1,900 an ounce. And quality gold stocks are taking off as well.

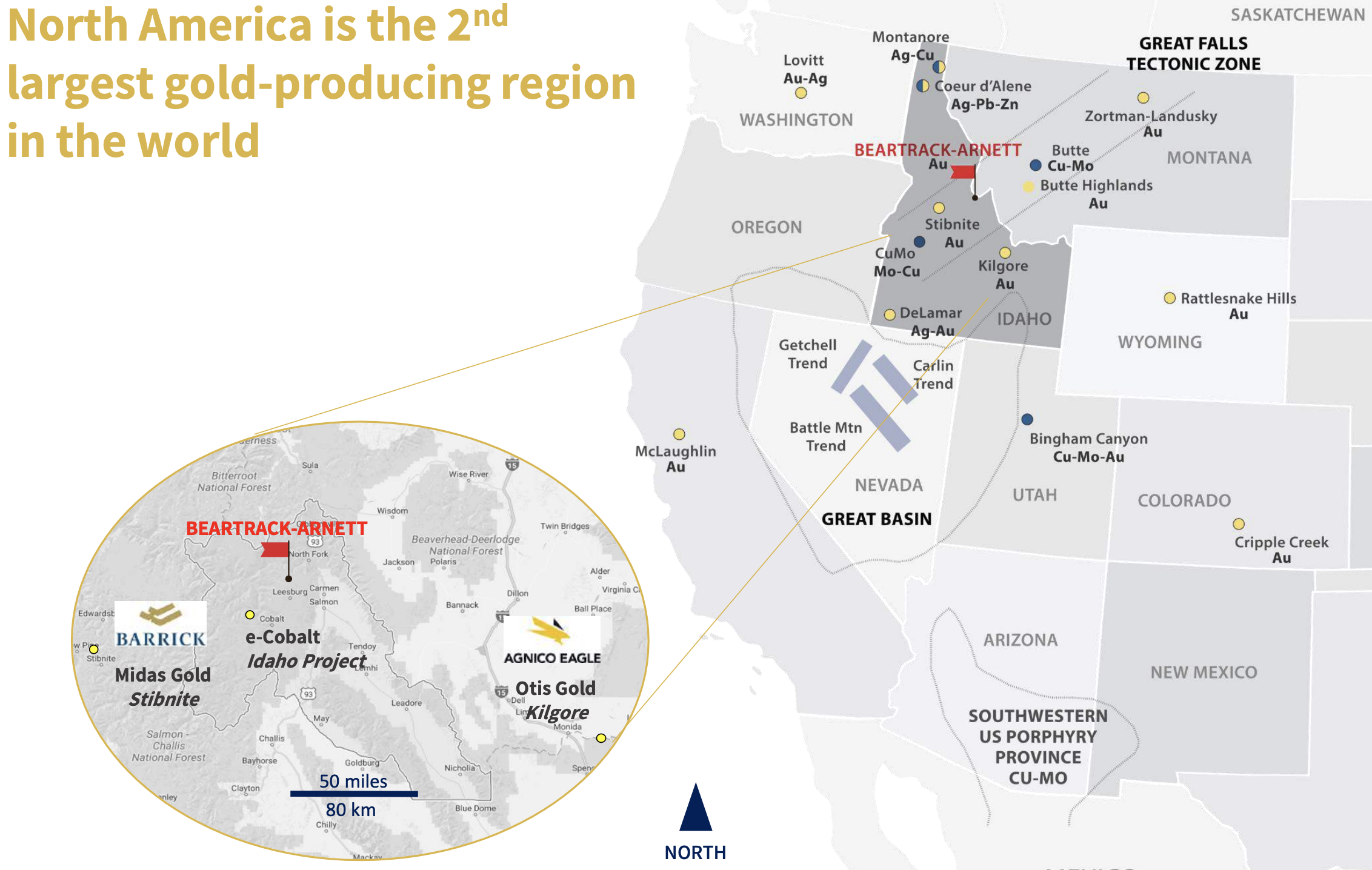

Revival Gold – which is currently trading around C$1.00 per share on the Toronto Venture Exchange under the symbol RVG – just announced it’s evaluating the heap leach potential of its Beartrack-Arnett Project, Idaho.

Now is a perfect time for investors to start looking at Revival Gold:

- Revival Gold is proceeding with a preliminary economic assessment

- This comes after a recent resource update increased the gold resource for the project to 3 million ounces

- Revival is also in the middle of a 10,000 meter drill campaign with results ongoing

- Revival is now one step closer to restarting the Beartrack Gold Mine

- READ: My interview with Revival’s president & CEO, Hugh Agro

This updated resource of 3 million ounces of gold at Beartrack-Arnett, may be all that’s required for Revival to officially announce the planned restart of the Beartrack Gold Mine, located in Lemhi County, Idaho.

That would mark a very important development for a US gold market that just recently turned the corner.

You see, Beartrack is a past-producing open pit heap leach mine that was operated by Meridian Gold [now Yamana Gold; NYSE: AUY] and produced roughly 600,000 gold ounces. The mine was closed in 2000 as a result of low gold prices, below US$300 an ounce.

The days of cheap gold are history; the yellow metal is now more than 6X those levels!

Hence, it’s easy to see the Beartrack/Arnett opportunity for Revival Gold AND for investors seeking to gain exposure to an emerging gold area play in one of the safest mining jurisdictions in the world — the United States, and specifically, Idaho.

From an individual investor standpoint, it’s critical to understand that Beartrack is a classic advanced-stage “brownfield” gold project. This brings with it a number of important advantages over the typical “greenfield” mineral exploration project — including reduced risk, huge discounts on capital costs, and a shorter time horizon from exploration to production:

- A key defining advantage of a brownfield project is the vast amount of available exploration data, which derisks many aspects of the project while offering immense economic benefits to both the company and its shareholders.

- Brownfield projects range from advanced development stage with a known resource...all the way to proven producer.

- Greenfield exploration projects carry the risk of operating in literally uncharted territory, typically with very limited geophysical data and drilling (if any).

- The Revival Gold team has a firm understanding of these advantages and has them in-play for RVG shareholders.

The GOLD is THERE!

The state of Idaho has a long and distinguished record of placer gold production and is considered among the most mining-friendly US states. Placer gold was discovered in the Napias Creek drainage after the Civil War with estimated placer production between 400,000 and 600,000 ounces of gold.

A 30-stamp mill was put into operation at Arnett around the turn of the last century but there was little lode production from the project area until the Beartrack deposit was put into production in the late 1990’s.

Beartrack – which is located in Lemhi County, east-central Idaho, approximately 13 miles northwest of Salmon – had life-of-mine production of approximately 600,000 ounces of gold during its initial run...before low gold prices below $300/oz forced its closure.

Times have changed: Gold is over $1,900 an ounce. Revival Gold controls the Beartrack-Arnett Project. $Billions in gold were left behind!

At present, Beartrack-Arnett boasts a current resource estimate of 1.35 million ounces at 1.16 grams per tonne gold indicated and 1.64 million ounces at 1.08 grams per tonne gold inferred for a total of 2.99 million ounces of gold.

That’s a very substantial near-surface gold resource...one that few junior gold companies ever achieve. Again, it’s one of those distinct advantages brownfield projects hold over their greenfield counterparts! Also impressive is that greater than 60% of the resource is in the “indicated” category.

At current gold prices above $1,900 per ounce, 2.99 million ounces of above ground gold has a value of more than US$5.0 billion.

Revival is aiming to advance toward a preliminary resource estimate of leachable gold material at Arnett. That material would then be trucked to existing infrastructure at Beartrack — yet another huge cost advantage for Revival Gold.

As you can see, there’s a lot of exciting things in-play right now with Revival Gold. We’re at a crucial development stage for the company, and the drills will soon reveal even more about the underground prize.

I had the opportunity to sit down with Revival’s president and CEO, Hugh Agro. Hugh is a former Executive VP at Kinross (NYSE: KGC), where he was instrumental in the company’s growth initiatives in Russia. He is also a former executive with Placer Dome.

Needless to say, he knows his way around a precious metals deposit. Please enjoy the interview.

Interview: Hugh Agro, president & CEO of Revival Gold

Mike Fagan: Good morning, Hugh, and thank you for taking the time to meet with me today. There’s obviously a ton going on with Revival Gold right now. Let’s start with the resource update that came out earlier in 2020.

Hugh Agro: Thanks for having me, Mike. It takes a lot of expertise to do this kind of work and it's something that we've been busy at for a number of months here now. We've got a super explorationist in Steve Preismeyer, our VP of Exploration. Our General Manager, Pete Blakeley, former General Manager for the operation at Beartrack. So a lot of in depth knowledge and an understanding.

At the board level we've got folks like Wayne Hubert, our Chairman who's done it before and with Andean Resources. Don Birak, Idaho resident and a long-time and well-regarded explorationist across the Cordilleran. This kind of guidance and strategic leadership is what makes all the difference for Revival Gold.

Then we've got the input of our consultants, Roscoe Postle Associates, a really well-regarded firm that did this resource update and all the analysis behind it, including on the metallurgical side with input from SGS and from John Marsden. A really good team and thank you for recognizing the efforts of the team and of the work that's come from it.

Yes, there's lots of detail there and we are very methodical. But as we know in the mining industry, there's lots of things that can go wrong so you want to make sure you've covered all the bases. I think we've done that with this release.

3 million ounces is the resource number. But if you kind of dig down into it a little further, you can see that we've got a big quantity of leachable material in the order of 600,000 ounces. That's the relatively quick opportunity for us to potentially produce gold from this project. And then in the longer term, we've got this large and growing mill resource, which puts us on a really different level in terms of the scale of the project. And recognizing that there's only five gold mines in all of the United States that produce more than 300,000 ounces a year, this is important. And the scale that we've developed and that we're looking at and conceptualizing for Beartrack and the mill scenario puts us in that league.

MF: Congrats on that big increase in gold resources. But I have to ask, is there even more exploration potential there?

HA: It is substantial and it's quite obvious to the educated folks who get out to the project that we have this potential. We've now locked up 5,400 hectares, over 12,000 acres of land, including about 11 kilometers of favorable strike in the Beartrack Panther Creek Shear Zone. We know that over 5 kilometers of that's mineralized. We have, as you've said, close to 3 million ounces in that system and then the balance at Arnett. But we've got another doubling of the strike potential in the property position.

Furthermore, we have drill permits in the main area and we have additional permits coming into play for this year. Lots of catalysts ahead for growing the resource, growing the potential economics of the project, not just through the drill bit, but as you pointed out at the outset, we'll move to economics on the leach restart project. And given the brownfield nature and the existing plant infrastructure that's there, I think we have a head start to potentially producing cashflow from this project.

MF: You’re in the middle of an expanded 10,000 meter drill campaign. Can you discuss the results that have come out so far?

HA: You bet. So just 7 holes released so far, all with leachable material close to surface in the Haidee target area, which is, of course, a satellite deposit to what we have at Beartrack. This is exciting for us because it extends the mineralized envelope from beyond what we have in resource there, which is a modest 200,000 ounces. We're really pleased with the way that those first 7 holes have come out.

The balance 23 holes that are to come will add to the resource along the flanks of the deposit, as they've been laid out, assuming we again hit mineralization, which I believe we will. In total, 30 holes in the Haidee area.

The main conduit for mineralizing fluids at Beartrack is the Panther Creek Shear Zone. Currently we know it to be about 5.6 kilometers or just over 3 miles long and mineralized across that distance. It's important because where we intersect the Panther Creek Shear Zone, we tend to find mineralization. We tend to find a lot of it. That's the importance of that geological feature.

I should say we have three drill targets along the Panther Creek Shear Zone and extensions of the Panther Creek Shear Zone planned for this year at Beartrack.

We've got the drilling at the very south end of the property position at Rabbit, which is over a mile and a half from the footprint of the resource at Beartrack. We've got drilling at Joss, which is currently underway at the end of the footprint of the resource. And we've got this spot between the North and South Pits, which is an obvious bullseye.

Our track record to date is that we've hit in every hole we've drilled, but one. So expectations are high and our team is excited to be on the program this year and we'll look forward to getting those results to you as they come.

MF: Sticking with the properties, can you provide a quick overview of the significant infrastructure advantages that you have over some of your exploration peers?

HA: Yeah, maybe some context to start. There's two big gold companies in the universe of public gold companies. That's Barrick and Newmont, of course. There's another half dozen above $10 billion market cap in the space. And then beneath that, you've got three dozen producing companies, gold or silver, that are beneath $10 billion market cap and above a half a billion dollar market cap. And then another three dozen below that.

There's six dozen gold producers who, if they're not looking to replace reserves, are looking to grow their reserves and their resources as they try and sustain their businesses. I think that's a healthy market for us to look to beyond our institutional equity investor base that we chase after and the retail and family offices. So lots of investors for us to potentially speak to about this project who are looking for gold exposure in the United States, safe geography. I think that's the key here is we've got to get out and get this message of the scale, the magnitude, the importance of this project out to the broader audience.

MF: You just announced that you've commenced your preliminary economic assessment (PEA) on Beartrack and Arnett. Can we speak to that a bit and then we'll talk about what the second half of this year is going to look like for Revival?

HA: We are very excited about the project portfolio we have, the compelling value we offer. The market is coming around as you've pointed out and we think we've got huge optionality here for investors on the 3 million ounces in the ground and the potential for us to leverage that existing infrastructure.

Job one is the PEA for this year and we don't have any restrictions on being able to complete that work. We think we'll have that all wrapped up by the end of the year. We announced the appointment of Wood PLC as lead consultants. We've got KC Harvey doing the environmental and mine permitting related preparations for that PEA. And we've got a super gentleman by the name of Rod Cooper who is overseeing the effort for Revival Gold on the owner's team. A very experienced engineer who's built, managed, run projects all over the world and is a senior technical advisor to Revival Gold. So we've got the right team, we've got the right sort of work for the current workplace restrictions that are underway, and we've got the right asset for this market.

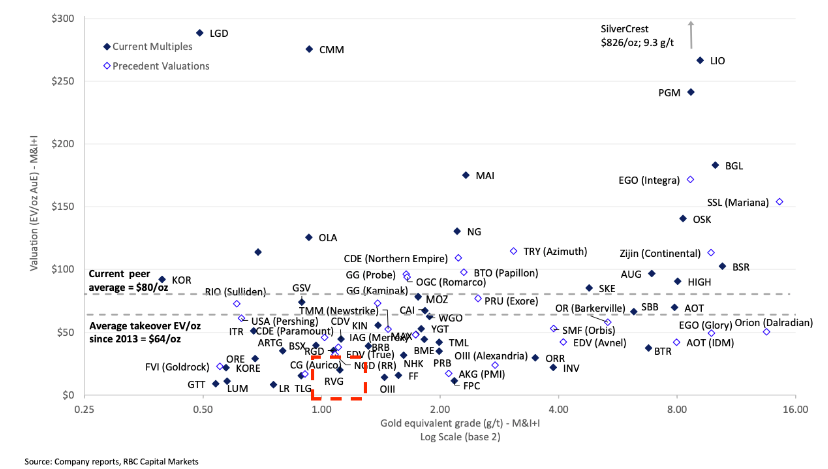

MF: Your shares are currently trading around C$1.00. There's price targets of over C$2.00 by several analysts. Your peer group average per ounce is right around the $48 per ounce, that's US, level. Based on that, your stock should be trading at closer to C$3.50. That's the opportunity. That's if you never find another ounce of gold, which of course is not likely. How do you address that pricing disconnect?

HA: The big part of the reason why we trade inexpensively is that we've got a really solid core of shareholders. They're not active traders. They're long-term investors like Orion Mine Finance and others. Management owns a big part of this company. There's no impatience on the part of our big shareholders with what we're doing and how we're building value over the long run. I think that probably means we're less likely to be on the radar screen of some of the active traders.

But the other thing is that I think it's a matter that we all face in this industry, which is size really does matter and liquidity begets liquidity. So alongside our work on building out the value in Beartrack-Arnett, we continue to look at opportunities to grow the business, build out our portfolio. And we think this is a good market to be doing that. Others recognize the importance of those steps and those opportunities to add value inorganically by seeking out like-minded partners. So you can bet we've got a lot of work going on on that front as well.

MF: Switching gears a bit, you have extensive background working with major gold producers such as Kinross and Placer Dome. Can you tell me about that experience and how it relates to what you’re doing now as president and CEO of Revival Gold?

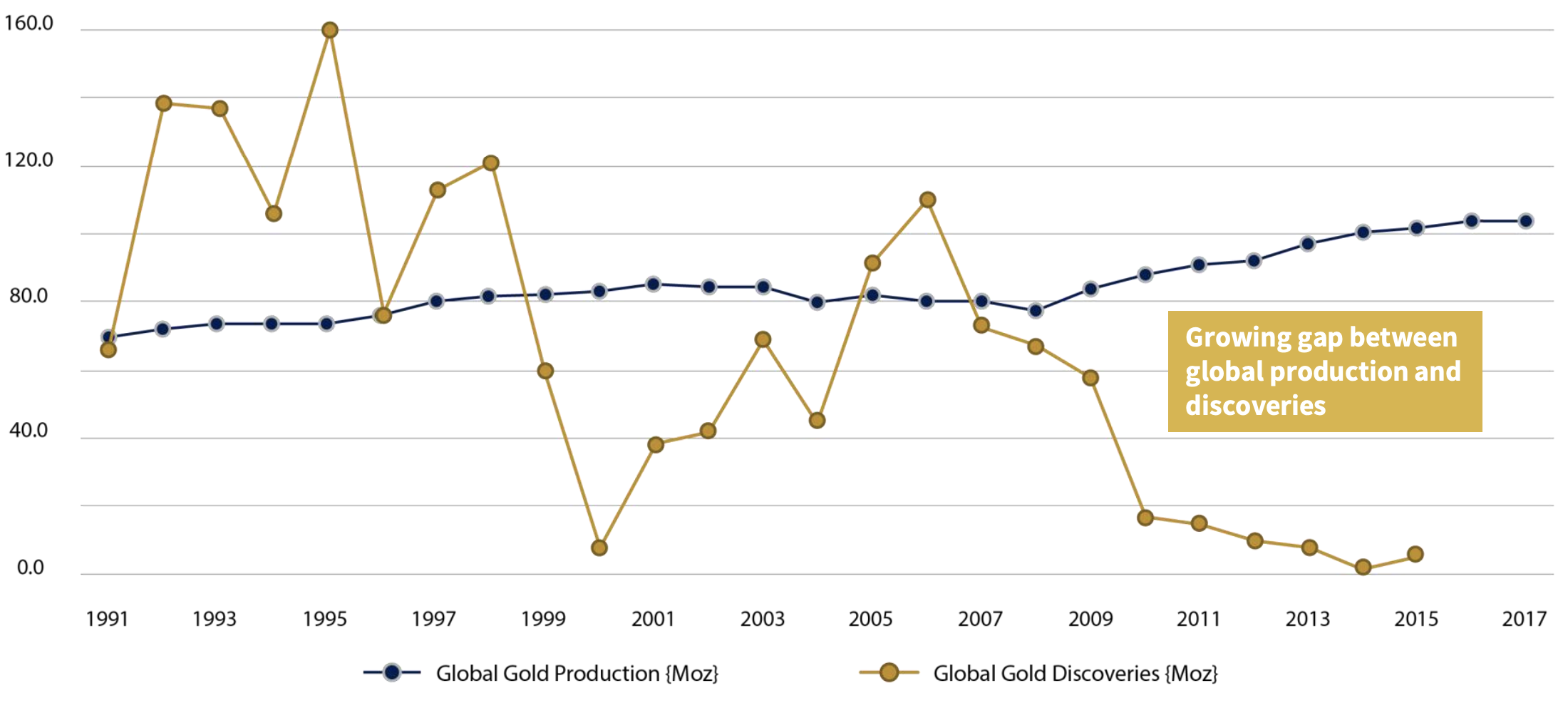

HA: I’m a mining engineer with a business development focal point. I’ve worked in growth, in gold, around the world for most of my 30-year career in mining. This combination of technical and corporate experience gives me a unique perspective on the current opportunity arising for investors as a result of the large and growing gap that has opened between the pace of global gold production and the availability of new gold production opportunities to meet future demand.

In late 2009, I retired from the gold business near the top of the last cycle having been part of the executive team at Kinross that took the company from a market cap of $1.7 billion to $17 billion. The timing turned out to have been very good. I stayed active on the board of a couple of juniors including Victoria Gold and Americas Silver, but I knew that I would return at some point to a full-time role in the business. It was just a matter of choosing the right time and the right opportunity.

All the training and experience I’ve had with senior gold producers such as Kinross and Placer Dome over the last three decades, along with participating in three metal price cycles, has taught me that timing and opportunity are key. In order to be able to recognize and act on the right opportunity, it’s also vitally important to have the right team. And, since no one can say with certainty when a price cycle will turn, one must be supported with long-term capital in order to survive a protracted downturn.

We have all of that with Revival Gold and more: Great timing [having been launched close to the cycle bottom in early 2017], a brownfield gold asset with an asymmetric balance weighted towards reward over risk, a veteran gold team with an impressive record of delivering for shareholders, and solid financial backing from the likes of US Global, Gold2000, and Orion Mine Finance.

MF: Hugh, it’s been a fascinating discussion, and I thank you once again for taking the time. Wrapping things up, is there anything you’d like to say to current and future Revival Gold shareholders in terms of what they might expect news wise over the coming months?

HA: Thank you as well, Mike. It’s been an absolute pleasure.

We have a busy 6 to 9 months ahead of us, and Revival Gold shareholders can most certainly expect a steady stream of news!

The Opportunity

Revival Gold remains largely undiscovered by Wall Street and undervalued as well — giving investors a timely opportunity to get involved in RVG at this exciting development stage.

The company’s roughly 71.2 million outstanding shares are currently trading around C$1.00, giving it a market cap of just C$72 million.

The chart (below) reveals that Revival Gold is trading at the low end of the spectrum relative to the current amount of measured and indicated gold it controls.

That means RVG could trade much higher in the near-term.

Specifically, as Revival Gold continues to add significant gold ounces by way of the drill – while simultaneously advancing its Beartrack/Arnett project toward production – it seems inevitable that the stock will undergo a substantial rerating to the upside in order to compare more equally with its peer group.

I have no doubt that major US miners are keeping a close eye on Revival Gold and its pending mine restart at Beartrack.

It’s the kind of brownfield operation that could have large implications across the gold sector as mining firms seek to reignite other past producing mines across North America and globally in the current $1,900+ per ounce gold market.

As a formerly producing mine, Beartrack offers numerous valuable advantages over the typical greenfield exploration project, including a maiden two million ounce gold resource, an 11,000 sq ft core facility, leach ponds, and existing power and water. And the property lies just 10 miles from the town of Salmon, Idaho, making for an easy drive with roads all the way into the main project area.

At Beartrack/Arnett, we already know the gold is there! And analysts are starting to pay attention:

With the 3 million ounce resource and the potential for Revival to add significant gold ounces at Beartrack/Arnett, renowned research analytics firms Paradigm Capital and Beacon Securities recently put out price targets of US$1.85 and US$2.00 per RVG share, respectively.

Those price targets are up to DOUBLE what Revival Gold currently trades…and they may prove conservative.

Learn more about Revival Gold and sign up to its investor list by clicking here.

And click here to get real-time updates from the company on their Twitter feed.

CLICK HERE FOR THE MOST RECENT INVESTOR PRESENTATION

Yours in profits,

Mike Fagan Editor, Resource Stock Digest