Skyharbour

Resources Ltd.

SYH | SYHBF

Building a High-Grade Uranium Resource

in Canada’s Athabasca Basin

Skyharbour Resources (TSX-V: SYH | US-OTC: SYHBF) is a preeminent uranium exploration company with projects located in the prolific Athabasca Basin of Saskatchewan, Canada.

With its own flagship project and several projects being explored by partners, Skyharbour Resources Ltd. – currently trading around US$0.25 per share – represents an intriguing speculation in the North American uranium exploration space.

Flagship Property: Moore Uranium Project

Skyharbour owns 100% of the 137 square mile Moore Uranium Project located 9 miles east of Denison’s Wheeler River Uranium Project and 24 miles south of Cameco’s McArthur River Mine — all located in Canada’s famed Athabasca Basin.

This is some of the richest uranium ground on earth!

In July 2016, Skyharbour secured an option from Denison Mines (TSX: DML) (NYSE: DNN), a large strategic shareholder of Skyharbour, to acquire a 100% interest in the Moore Uranium Project which hosts the high-grade Maverick Zone — a key area of interest.

Skyharbour Resources is generating news from its drill program at Moore, as well as from its partner-operated projects in coming months.

| Flagship Moore Uranium Project hosts high-grade U3O8 mineralization at the Main Maverick Zone – discovered by JNR Resources in the early 2000’s | |||

| Historical drill results include 4.03% U3O8 equivalent over 10 meters – including 20% U3O8 equivalent over 1.4 meters at a depth of just 265 meters | |||

| Newly discovered high-grade mineralized lens at Maverick Zone illustrates strong discovery potential for additional high-grade lenses along strike | |||

| Only 2 km of the total 4 km long Maverick corridor has been systematically drill-tested leaving robust discovery potential along strike as well as at-depth | |||

| READ BELOW: My exclusive interview with Skyharbour CEO: JORDAN TRIMBLE | |||

Uranium Prices: Breaking Out!

In the resource space — timing is everything!

After a near decade-long bear market in uranium, we’re finally starting to see U3O8 prices breaking to the upside primarily as a result of a wave of temporary mine closures due to the coronavirus pandemic – most notably the suspension of operations at Cameco’s massive Cigar Lake uranium mine and production curtailment at Kazakh mines.

We’ve seen U3O8 prices surge from around $25 per pound to above $33 a pound… signaling what could be the start of a long-awaited breakout for this vitally important, clean energy metal — commonly referred to as yellowcake.

Some analysts believe the COVID-19 crisis could create a shock to the nuclear fuel supply chain causing a substantial rise in U3O8 prices as large producers suspend operations, draw down inventories, and/or increase market purchases to fulfill existing contractual obligations with utilities.

VIII Capital said in a research note that in the United States, where 24% of the uranium used for nuclear fuel comes from Canada, it “suddenly looks like the [utilities] will be scrambling for product, as the largest source of uranium is gone.”

The virus is also slowing production in Kazakhstan — which supplies over 40% of global uranium.

Developments such as these could drive uranium prices significantly higher in the weeks and months ahead.

I’ve done my due diligence on Skyharbour Resources…

And I’m impressed with the company’s vast uranium property portfolio in the Athabasca, its partnerships with global uranium development companies, and its highly-adept management team starting with CEO, Jordan Trimble, and head geologist, Rick Kusmirski.

Noteworthy is that Rick Kusmirski has been a uranium-focused exploration geologist for some 4-plus decades — previously serving as exploration manager at industry leader Cameco for 10-plus years.

Skyharbour boasts a highly impressive team — one I firmly believe has what it takes to get the job done for SYH / SYHBF shareholders.

Please enjoy my exclusive interview with Skyharbour’s President & CEO, Jordan Trimble.

Exclusive Interview: Jordan Trimble, CEO,

Skyharbour Resources Ltd.

Mike Fagan: Jordan, thank you for taking the time today. Definitely lots of exciting drilling and exploration news to get to on multiple projects. But first, let’s take a brief step back and begin with an overview of Skyharbour Resources and its multifaceted strategy of high-grade uranium project development in Saskatchewan’s prolific Athabasca Basin.

Jordan Trimble: Absolutely, Mike… and great to be with you as well. As you know, Skyharbour started about 6 years ago. At that time, we saw a real opportunity to begin piecing together a large, project portfolio of high-grade uranium projects in the Athabasca Basin.

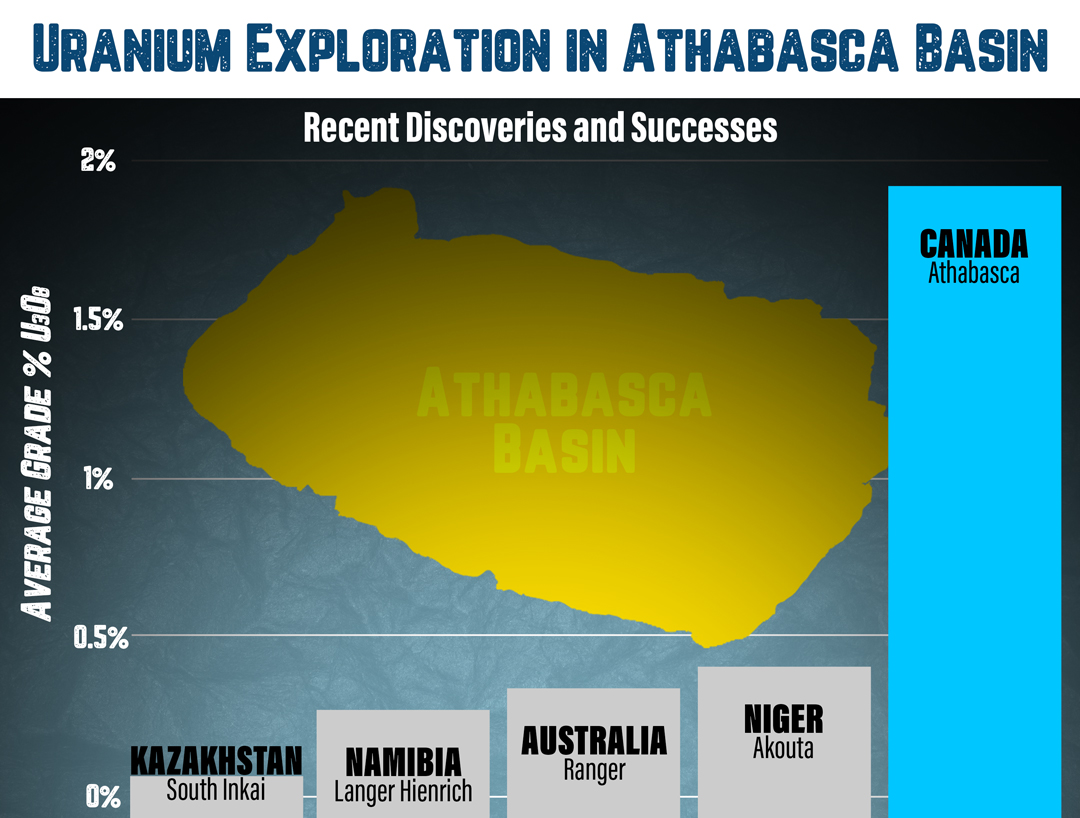

The Athabasca Basin is the Saudi Arabia of uranium.

It’s the highest grade depository of uranium in the world with major deposits including Cameco’s McArthur River Mine (the world’s largest high-grade uranium deposit) and Cigar Lake Mine, Nexgen’s Arrow Project, Fission’s PLS Project, and Denison’s Wheeler River Uranium Project which includes the high-grade Phoenix and Gryphon deposits.

Turning to today, as a highly-experienced and focused team, we have been very opportunistic in a uranium market that’s just now starting to show some signs of life. We’ve acquired a total of 6 projects scattered throughout the Athabasca Basin at various stages of exploration and early-stage development.

Best of all, we’ve acquired this very sizable project portfolio for about C$5 million with a good chunk of that paid in stock. From a valuation standpoint, these projects have had almost C$90 million in historical exploration and development work on them.

Two of the projects were in a company that was run by my head geologist, Rick Kusmirski, called JNR Resources: Moore and Falcon Point, both of which host uranium deposits.

JNR was trading at a $350 million market cap with those projects, so it shows the re-rating potential when we come back into a uranium bull market… which we may be seeing the early signs of now.

Our flagship project is the high-grade Moore Uranium Project which is located on the east side of the Athabasca Basin. And it’s important to note that the east side is where most of the existing mine infrastructure for the basin is located.

The Moore Uranium Project has been the focus for us over the last several years. We own 100% of it. We acquired the project several years back from our largest shareholder, Denison Mines. Denison is an important part of our story and their president and CEO, David Cates, is on our board. We have a very close working relationship with the Denison team.

We also have strategic partners on a few of our other uranium exploration projects.

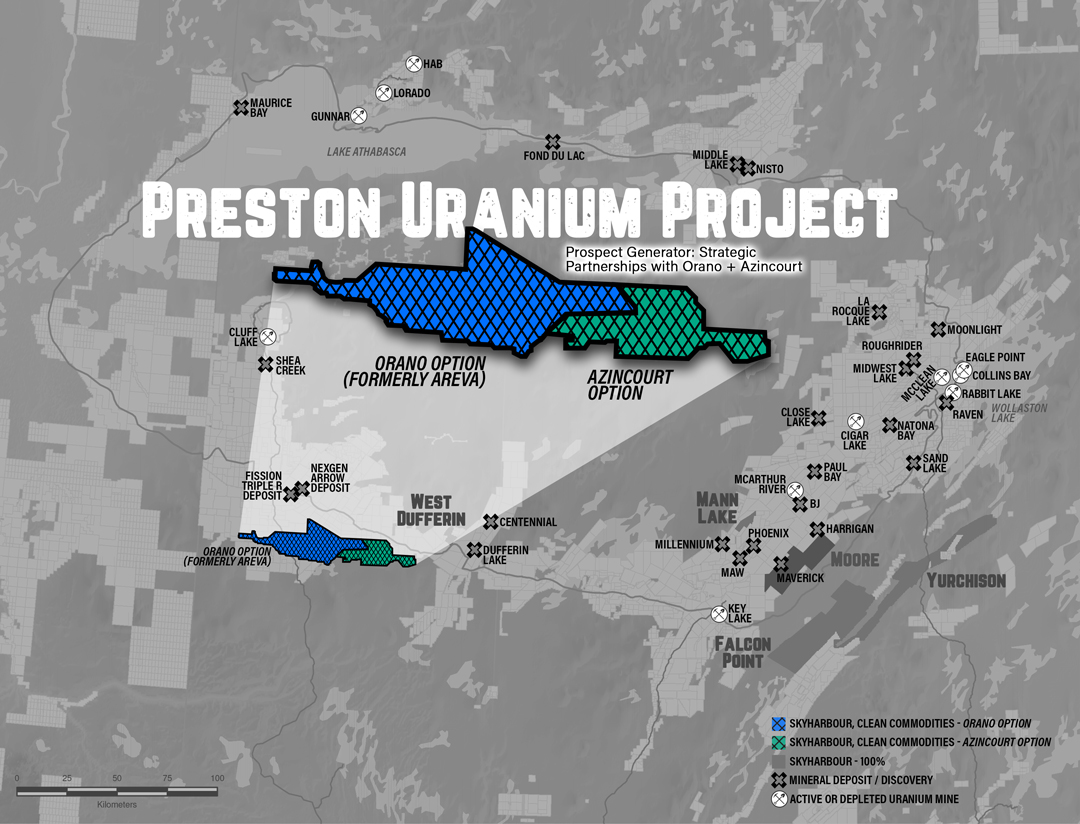

We’ve brought in a strategic partner, France’s state-run Orano — previously known as AREVA. Orano is France’s largest uranium mining and nuclear fuel cycle company. They’ve come in with an earn-in option at our Preston Uranium Project, which is over on the west side of the Athabasca adjacent to NexGen and Fission.

Their earn-in allows them to acquire up to 70% of the project by spending up to C$8 million; that’s C$7.3 million in exploration expenditures and C$700,000 in cash payments.

They’re about halfway through the earn-in as we speak and have recently completed a large geophysical program. We have a similar deal with Azincourt Energy at our East Preston Project whereby Azincourt can acquire 70% of the project by spending C$2.5 million and making $1 million in cash payments.

We also have a deal whereby Australian company Valor Resources can earn 80% of the North Falcon Point. I'll just note that that's the northern, essentially half, of our Falcon Point project. So we still retain the southern half, which has the deposit on it. The northern half, we will option out to Valor here. The terms of the deal, $3.5 million in exploration expenditures over a 3-year period and just under half a million in cash payments, as well as 250 million shares.

These partnerships, which are key to our prospector generator model, serve as a sound and strategic way for us to ensure our projects are being advanced. In this case, they're being advanced using other people's money.

It also helps by bringing in some cash for us. We get cash payments from these partner companies as they earn-in on the project, which helps us to keep the equity dilution down. It allows us to focus our time, money, and efforts on our flagship Moore Uranium Project as well as our other core projects in the Athabasca.

MF: Definitely, always a plus when you can use other people’s money! So, Saskatchewan’s Athabasca Basin is without a doubt the hotbed of uranium mining in North America. What are some of the key benefits of working in that province?

JT: Well, Mike, Saskatchewan is one of the best places in the world to work. It’s one of the top-ranked mining jurisdictions on the planet. It’s consistently ranked in the top five by the Fraser Institute. In the last study, it was ranked number three globally… and there’s a number of important reasons for that.

Obviously, there’s great mineral endowment. It’s not just uranium; there’s potash as well as a veritable treasure trove of precious and base metals.

And you have the added benefit of a pro-business provincial government. You have a long and prosperous history of mining in the province… in particular uranium mining.

It’s worth noting that one of the largest employers of First Nations and northern communities are the uranium companies like Cameco and Orano. And that goes a long way in the overall mine development process.

For instance, the permitting process – whether it’s for exploration, development, or production – is relatively transparent and clearly defined. You know exactly what you’re dealing with… very few surprises, so to speak.

As you know, Mike, there are tons of mining jurisdictions around the globe where you simply do not have that sort of transparency and pro-business environment.

All of those things in combination are the reason why Saskatchewan is consistently ranked so high by the Fraser Institute and why it attracts massive investment from top-tier mining companies year-in and year-out.

MF: Excellent! Jordan, you’ve got a lot of different projects going at Skyharbour; what can you tell me about the overall potential of the company’s current uranium project asset base? And are you also seeking additional acquisitions at this time?

JT: We’ve done a really good job at being opportunistic on the acquisition front, Mike. That really has been a key strategy for us in our portfolio advancement model.

We recognized, early on, that there are very few companies that are truly active in our space, which is in itself an opportunity to go and consolidate assets and value-add these projects with top-tier teams.

So we’ve done a good job of building the project portfolio relatively inexpensively… acquiring projects for literally pennies on the dollar.

We talked about the numbers a bit: C$5 million spent and about C$90 million in historical exploration and development work invested in our projects. At one point, a couple of our current projects were in a company valued at over C$350 million when uranium was trading at its highs in 2007.

Plus, we’re always evaluating new potential acquisition opportunities.

In fact, we have been actively staking and adding acres to one of our existing projects, called Yurchison, on the east side of the Athabasca Basin. There’s another nearby project called Janice Lake that Rio Tinto recently optioned from a company called Forum. They have a $30 million earn-in deal with Rio Tinto, which is one of the world’s largest mining companies. So there’s quite a bit of interest in that area right now.

Plus, we’re doing some additional staking along the south border / central part of the Athabasca. In all, we’re continuing to add to our robust uranium project portfolio in literally the best place in the world to explore for and mine yellowcake.

MF: What’s the discovery process like in the Athabasca; it’s no longer just “drill and hope” is it?

JT: No, definitely not! In fact, that’s one of the main reasons why – when we started the company – we were able to essentially follow some of the recent discoveries made in the basin… discoveries made by Fission at PLS, by Hathor at Roughrider, by Denison with the Phoenix and Gryphon deposits, and by NexGen with the Arrow Deposit.

There have been several notable recent high-grade discoveries and we are looking to add to that list.

We’re seeing new techniques and new methodologies being utilized in the discovery process, and for me, that’s always something I’m interested in: going into a proven brownfields jurisdiction – where there’s been a fair bit of historical exploration and development – and then applying some new thinking as it relates to the discovery process.

There’s been a couple of big breakthroughs that have led to a slew of new discoveries being made over the last 15 years in the Athabasca. One of which is companies looking for and drilling targets in the underlying basement rock.

For a very basic summary of the geology, the Athabasca Basin is a sedimentary basin which was once an intercontinental lake which has since been filled in.

Think of it as a big bowl filled with sedimentary sandstone rock. And below that and around that is what we call the underlying crystalline basement rock. The contact between the sandstone and that surrounding hard rock is called the unconformity — a very important geological term in the Athabasca Basin.

Mike, a lot of the historical drilling and discoveries that were made as a result were in the sandstone or at the unconformity (the contact). Far less work historically had been done drilling into the underlying basement rock.

More recently, we’re seeing companies focusing more of their efforts drilling into the underlying basement rock or outside of the sandstone cover. The importance being that the high-grade mineralizations come up from below. Thus, you’re getting the feeder zones that create these deposits, which can host very high-grade mineralization.

These are incredibly rich high-grade deposits, and they’re basement hosted.

Compare that to McArthur River, for example, which was discovered after about 200 drill holes. If you look at the discovery cost on that, it’s a huge price tag. Of course, it’s an incredible deposit; it’s worth billions of dollars. But it’s very difficult and simply not practical or feasible for a junior mining company to go about making a discovery via that methodology of wildcat drilling.

A junior company would likely go bankrupt well before making that sort of find. So things have changed. We now have much more refined, deeper penetrating, and highly-targeted geophysics that are allowing us to gain a better idea, a clearer image, of what’s happening geologically at-depth.

We’re using drone-flown geophysical surveys, which are providing us with new targets as well as more refined existing targets at a lower cost in the underlying basement rocks. And that has been the recent focus for Skyharbour’s drilling.

At our flagship Moore Uranium Project, the enhanced geophysical surveys in addition to improved geological modelling and understanding are providing us with these higher-priority, basement-hosted targets that we previously didn’t have a good handle on. So advancement in geophysics as well as in other exploration techniques is really proving to be a game-changer for us.

Essentially, it’s a combination of new approaches and advancements in existing techniques that’s allowing us to go out and make new discoveries in the Athabasca without having to drill hundreds upon hundreds of deep and expensive drill holes.

MF: That’s fantastic! So, in the basin, are we talking primarily underground mining, or do you see potential for an open-pit component as well?

JT: In the Athabasca, it’s typically underground mining, Mike. There have been some open-pit mines, but most of the recent discoveries would be mined through conventional underground mining.

However, not so dissimilar to new techniques and methodologies being used to improve the discovery process in the basin, there are several new mining methods being proposed and two in particular we’re closely watching that could have a positive impact on several uranium projects in the basin.

One, Denison Mines, again our largest strategic shareholder, is proposing using ISR (In-Situ Recovery) at their Phoenix deposit, which is very interesting. For Denison, it could mean potentially becoming the lowest-cost uranium producer in the world.

For those not familiar with ISR, it’s where you drill injection wells and then install recovery wells. You’re essentially injecting a solution down into the ground that has an affinity for uranium. Uranium then latches on, and the recovery wells bring the uranium solution up to the surface where a separation process takes place to ultimately produce yellowcake.

At surface, the processing is relatively straightforward. Plus, you’re not having to spend a lot of money building a conventional mine and associated infrastructure. ISR has the potential to bring costs down tremendously. And because it has a much smaller environmental footprint, the permitting timeline to production could potentially be much shorter.

ISR hasn’t been used yet in the Athabasca Basin; however, it’s used widely in the US and in Kazakhstan; Kazakhstan being the largest producer of uranium globally. So, it’s a method that is proven in other parts of the world and accounts for a significant amount of annual uranium production.

If ISR works as well as it appears it could in the basin, this could be a game-changer for several projects and deposits as well as for new discoveries going forward.

Second, a new mining method specific to Athabasca Basin uranium deposits is called SABRE (Surface Access Borehole Resource Extraction), and it’s being developed by two partner companies of ours; Denison and Orano.

It is still in its developmental phase but, as the name implies, it involves drilling boreholes from surface and then using a technique called jet-boring to break up the rock underground using high pressurized water and then pumping the uranium-water mixture up to the surface to be processed.

Using this new mining method, you could go in and selectively mine higher grade pods as well as potentially decrease costs — thereby reducing the timeline to production and simplifying the permitting process.

MF: Interesting… we’ll certainly be keeping an eye on the progress made with these new exploration and mining methods in the basin.

Would you mind, Jordan, going into your background a bit… and also the experience of some of your key personnel?

JT: Yeah, absolutely, Mike. I’ve been working in the industry for about 10 years now. I started at a gold company called Bayfield Ventures. I was doing corporate development for Bayfield when it was a small exploration company with gold projects in Ontario. I was fortunate enough to come in right before a pretty significant high-grade discovery was made at a project the company had in an area called Rainy River.

And it was our chairman here at Skyharbour, Jim Pettit, who was running Bayfield at that time. It was a great experience as we advanced the project from a high-grade discovery through resource delineation and ultimately sold it to a larger mining company called New Gold.

It’s now a large producing open pit mine called the Rainy River Mine. To make a long story short, we sold Bayfield just over six years ago, and that’s when I began running Skyharbour Resources.

I partnered with my head geologist, Rick Kusmirski, who lives in Saskatoon. Rick has a notable mining pedigree; he’s been an exploration geologist focused on uranium exploration for over 40 years and has been involved in several notable discoveries.

He was the exploration manager at industry-leader Cameco for over 10 years. After that, he started his own company, JNR, which he took from C$0.05 to over C$4 per share between 1999 and 2007.

JNR made a number of discoveries and was ultimately acquired by Denison Mines. It was shortly after that, I connected with Rick and we started to build a new uranium company in Skyharbour.

To round out our board, Dave Cates, the president and CEO of NYSE and TSX listed Denison Mines, is a director of Skyharbour.

We also have Paul Matysek as a strategic advisor. Paul is very well-known in the industry having been credited with a handful of very significant successes.

He’s built and sold five mining companies over the last 12 years. His biggest win was a uranium company called Energy Metals which he started in 2004 at a $10 million valuation and sold it to Uranium One three years later for $1.8 billion.

So Paul knows a thing or two about building and selling mining companies.

MF: Excellent. So, let’s talk about the drill program at the flagship Moore uranium project.

JT: Things have gone quite well. Very, very pleased with the drilling. Again, the focus has been on the Maverick Corridor, looking for these higher grade feeder zones in the basement rocks. We really think we're onto something much larger there. We just put out some high grade results from there in early 2021, and are fully funded for another program this year as well, having raised money through one generalist funds last year.

There's still a lot of blue sky potential on this project. I do note that this is just one part of the 36,000 hectare land package, which comprises the Moore project, so there are other regional targets.

I will note we are planning to put out a resource estimate at some point. With every program that we've carried out, we've been adding to the high-grade known mineralization there in the sandstone and, more recently, in the basement rock. So an exciting program, big catalyst for us coming up. Again, we're going to compliment it with other programs, partner-funded programs, at some of our other projects including Preston and East Preston.

MF: Exciting. Can we talk about the other projects a bit?

JT: Yeah. In July 2020, our partner company, Azincourt, announced a summer program at our East Preston project. They're still carrying out some field work in geophysics, electromagnetic EM survey that they're going to be carrying out. This will suffice for the remaining $150,000 or so that they need to spend as per their earn-in requirement. They also had to make a $200,000 cash payment. Then they will have earned in 70%, will form a joint venture and continue advancing that project thereafter. They have plans for a drill program later this year, once they complete the summer field program.

Then at our Preston project, Orano, France's largest uranium mining and nuclear fuel cycle company, is exploring and advancing that project. We're just waiting to get the final report back from a field program that they carried out last year. We'll have some news out on that and plans going forward at that project.

Then just a quick note, as you're well aware, we have a large portfolio of projects scattered throughout the Athabasca basin. We employ the prospect generator model. We are in fairly advanced negotiations on, in particular, one of our other projects, looking at bringing in a third partner. So look out for news on that forthcoming.

MF: Jordan, what’s your overall take on the uranium market, and are you looking at any particular catalysts, such as the recent COVID-19 related mine closures, that could set some upward momentum in the uranium spot price?

JT: I do believe we’re at the very early stages of a recovery and bull market for uranium. And we’re definitely seeing a major supply side response play out as a result of the coronavirus pandemic and the temporary mine closures it’s causing in addition to closures prior to the pandemic.

Almost 50% of primary mine supply was offline at the peak of the pandemic in April and May. And there is potential for additional supply disruptions going forward due to the virus.

Naturally, it’s not how any of us would have envisioned nor welcomed a boost in uranium pricing but it has expedited what many industry experts were predicting would happen with underlying fundamentals having grown more bullish over the last several years. It’s also important to note that there was significant supply destruction prior to the pandemic as primary mine supply was forced to shut in due to low uranium prices and depleting reserves.

The recent temporary mine shutdowns – most notably the halt in production at Cameco’s Cigar Lake Uranium Mine as well as production curtailment in Kazakhstan – is helping to drive prices higher and will continue to do so if these haults are extended and/or if other large mines are forced to batten down the hatches as we work our way through this crisis.

If you look at previous cycles, for instance, where you saw a bottom put in place in the late-90’s and early-2000’s – and then from 2002 to about 2005 – you saw a consolidation happening. You could see the downtrend reversing… but it was by no means an immediate bounce back.

It wasn’t until 2006-07 when a confluence of factors, including a supply side shock involving a flood at the Cigar Lake mine, drove the uranium price substantially higher. The spot price got up to about $138 a pound – and pretty much every uranium equity went up multiples during that run.

We’re talking 10X, 20X, and even 30X returns on some of those companies.

If you look at the cycle we’re in now and the overall timing of the market, I think the bottom was put in-place in 2016 when we hit a low in the uranium spot market of just under $18 a pound.

At the moment, the metal price is trending higher due to changing market dynamics and a long awaited rebalancing. A major supply deficit is forming while demand is continuing to grow especially in nations like China and India. Uranium inventories are decreasing globally, while producers are having to purchase material in the spot market to make deliveries as per their utility contracts.

Cameco alone will have to purchase tens of millions of pounds of uranium this year as they are no longer producing at McArthur River and Cigar Lake which will put upward pressure on the spot price.

Furthermore, nuclear utilities can no longer bank on available uranium through the mid-term market as they have in the last few years as the carry-trade is unravelling with heightened volatility and decreasing mobile inventories. This will force them back to the table to negotiate longer term, higher priced contracts with the miners.

And lets not forget, it is the ONLY source of baseload, emissions-free, reliable, and cost-effective electricity generation. Public sentiment towards nuclear energy is improving as it serves the dual purpose of providing substantial amounts of clean electricity 24/7 while providing many jobs and a solid tax base.

The uranium spot price sat at about $25 a pound for several months, and now we’re ratcheting higher to over $30 per pound… so we’ll see where things go from here.

MF: In your opinion, Jordan, where do prices realistically need to head for increased investor interest and for North American companies to produce at a profit and for new development projects to come online?

JT: Mike, that depends on where you are in North America. The Athabasca Basin in Canada is the lowest cost producing region in the Western World. I think seeing the spot price breaking above $30/lb has begun attracting some traders, speculators, and new money into the space. However, I see a lot more upside here and I think if we see $40/lb, there will be a new wave of interest and buying coming into the market.

Just on the uranium market itself, when you look at the supply/demand fundamentals for the metal, it truly has, in my opinion, some of the most compelling fundamentals of any metal out there and we have the trend moving in the right direction.

You have a situation right now where demand is continuing to grow and, in particular, you have demand in places like China and India and other parts of the developing world where they’ve been building nuclear reactors very quickly on-time and on-budget.

There are over 440 current operable reactors, 55 reactors under construction, over 400 reactors ordered/planned/proposed globally. About a third of this growth is in China alone.

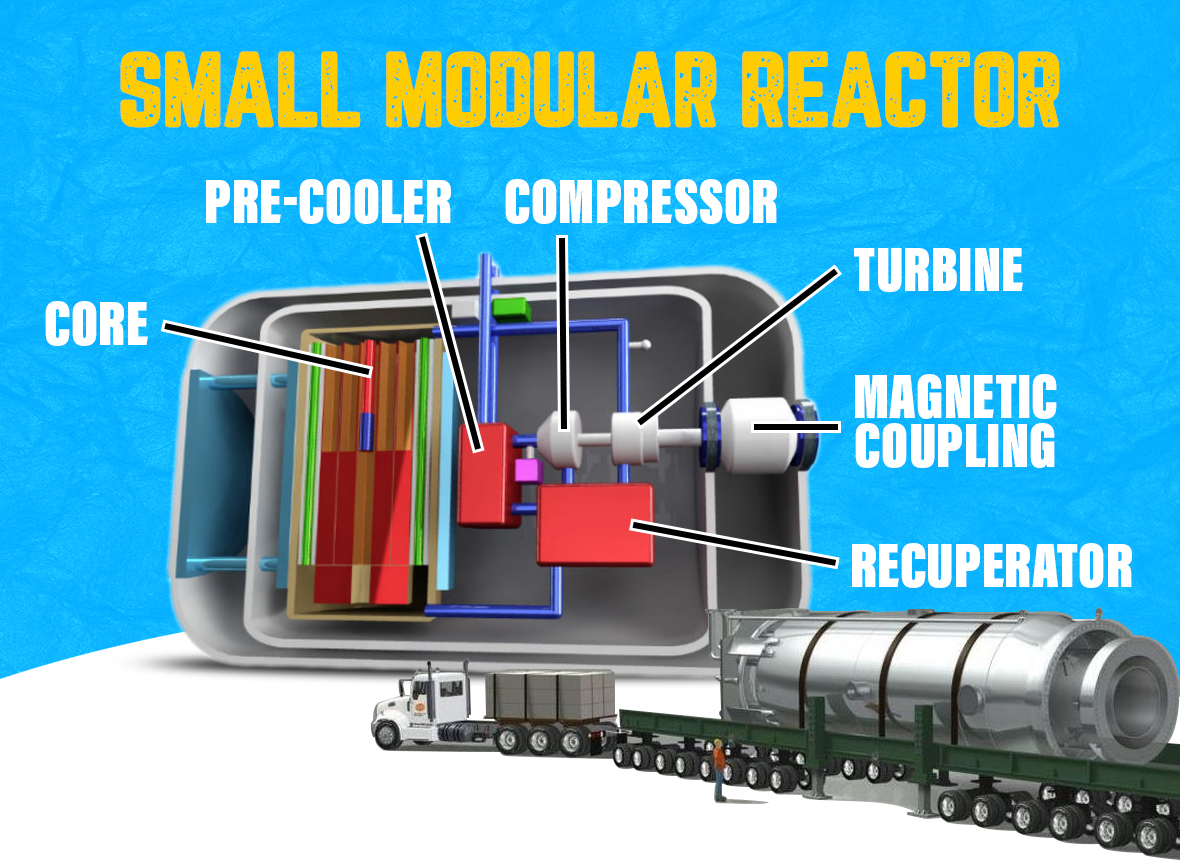

However, I see there possibly being robust new demand growth in developed countries going forward like the USA and Canada through new and advanced nuclear technologies like SMRs (Small Modular Reactors).

Recently here in Canada, we’ve had three provinces, including Ontario, sign a Memorandum of Understanding to expedite the development and commercialization of these Small Modular Reactors. So we could certainly see a decent amount of growth from that segment in the coming years.

There’s also been a major supply side response in the last three years to the low-price environment. There's very little production globally that makes money at current uranium prices… even with the recent surge to $30-plus per pound.

The key point is that we're trading well below the average all-in cost of production of $40 to $50 per pound. That’s really where prices need to head… ideally $50 to $60 per pound… to incentivize new production to come online.

A lot of analysts are forecasting $50 to $60/lb uranium, which is a big move from current prices.

Now getting down to the numbers, on the demand side, we currently see about 185 million pounds of annual U3O8 demand for nuclear reactors globally.

That number is continuing to increase, and it’s important to note that the demand side will be relatively sticky even through this pandemic as nuclear reactors will be some of the last power plants that would be shuttered if there is a meaningful decline in electricity consumption. It’s very costly to do so and utilities will look to lowering output at intermittent sources of electricity like wind and solar first.

On the supply side, we've gone from about 163 million pounds of primary mine supply in 2016 to about 140 million pounds that was expected in 2020 prior to the pandemic. Depending on how long the pandemic lasts, that 140 million pounds could decrease to well below 100 million pounds of annual supply.

When you crunch those numbers, you can see that there was a pretty significant primary mine supply deficit of over 40 million pounds looming, and it now looks like that number will continue to increase.

MF: Jordan, Kazakhstan, is the world's undisputed low-cost uranium producer, and market analysts have been concerned they can just continue to flood the market with cheap uranium. What's your take on that?

JT: Well, Kazakhstan is the lowest-cost uranium producing region in the world and is obviously a very big player accounting for about 40% of global primary mine supply.

The country’s U3O8 production numbers have really ramped up over the last 15 or so years – and the market pays close attention to everything they do.

For example, in early-2017, right after the bottom was put in-place, Kazakhstan announced an initial production cut. Just a few months after, we saw the U3O8 spot price jump up to the mid-$20s from the high-teens.

Uranium equities followed suit very quickly all the way from the Cameco’s of the world down to the junior explorers. We too witnessed a very fast equity value appreciation over that period of time.

So yes, the market is continuously monitoring Kazakhstan and their role as a major supplier and low-cost producer. However, they recently announced a reduction in annual production of approximately 20% due to production curtailment as a result of the virus.

All of the Kazakh production is ISR which requires sustaining capex and continual drilling of wellheads. That too has come to a grinding halt so there is concern that production will not be able to ramp right back up even after the pandemic ends, which could further tighten supply.

Furthermore, it doesn’t make much sense for them to flood the market even if they can. For starters, a higher uranium price benefits them as a newly-minted public company as they need to emphasize value over sheer volume and focus on profitability.

Secondly, we are seeing a growing push towards domestic, strategic, and secure supply chains especially in critical metals like uranium. This is the case for the largest consumer of uranium, America, and I highly doubt that US nuclear utilities are going to end up having to buy from only one supplier being Kazakhstan. They will want to maintain a more diverse contract portfolio including sourcing material from US and Canadian production.

We’re already seeing policy moving in this direction with the recent announcements around the Nuclear Fuel Working Group and a revitalization of the American nuclear industry. I think it’s important to note that Canada has been and will continue to be a reliable, safe, low cost source of uranium for US nuclear reactors.

MF: So in terms of nuclear’s global role in clean energy, Jordan, would you say sentiment is beginning to turn in favor of nuclear power generation?

JT: Yes, I’m definitely of the mindset that the green energy push is one of the big things that's going to continue to drive improved sentiment for nuclear power. Again, it’s the only source of base load, clean, affordable, reliable, and safe electricity generation.

Nuclear's role in combating climate change and improving air quality is going to be very important going forward, and we’re starting to see that narrative change in a positive way.

Even some well-known, previously anti-nuclear environmentalists are beginning to wake up to the realities of the modern world and the pragmatic solution nuclear provides.

One example is Michael Shellenberger who’s recently become one of nuclear's biggest proponents. He was Time magazine's Hero of the Environment in 2008.

Michael speaks often on the topic of nuclear energy, and one of the things that has changed his mind in favor of nuclear are the real life case studies and, quite simply, the facts.

For example, when we look at France and Germany, here are two countries that have gone in complete opposite directions with their energy policies. Post Fukushima, Germany announced that the country would phase out nuclear whilst making a major investment into “green, renewable energy,” which, of course, is an oxymoron given that nuclear is also emissions-free.

They've now invested over 160 billion Euros into renewable energy like wind and solar. Unfortunately, it hasn't panned out very well for them. There's been very little progress in reducing carbon emissions there. In fact, on a per kilowatt-hour basis, carbon emissions in neighboring France are about 10% of that of Germany.

Keep in mind, France is over 70% nuclear and stayed the course with nuclear.

Germany is now having to turn back on coal plants, lignite coal plants, which are heavy polluters. And when you look at the costs – not just the 160 billion Euro sunk cost into rolling out this green energy plan – you’ll see that Germany’s electricity costs are double that of neighboring France.

So emissions haven't gone anywhere, and, in fact, are going up in Germany yet their electricity costs are also going up significantly. This is something that a lot of pragmatic, practical environmentalists are pointing to and saying, "The numbers can’t be ignored." Bottom line is nuclear must play an important role going forward in combating climate change and improving air quality.

It’s simply a matter of energy density. We used to burn wood to generate energy, and then we burnt coal, and then oil and gas, all with increasing energy densities. Now we have uranium as the fuel in nuclear power plants, which has the highest energy density per unit of mass available for electricity generation.

Renewables like wind and solar rely on very dilute sources of energy which ultimately translates to massive amounts of land and materials needed to generate the equivalent amount of electricity that nuclear does. Typically wind and solar require 300 to 600 times more land to produce the same quantity of electricity when compared to nuclear power.

That is why we are seeing places like China, India, the Middle East, and even some African and South American nations rolling out their respective nuclear programs. We’re talking about large population centers that require a lot of power. Nuclear is the only clean-energy solution to power these cities and countries.

I think we’re going to continue to see a lot of well-known and respected thought leaders globally pushing for nuclear. Bill Gates has been a big pro-nuclear talking head for a while now and states, "Nuclear is ideal for dealing with climate change because it is the only carbon-free, scalable energy source that's available 24 hours a day.”

MF: Jordan, the audience should know that Skyharbour is a Canadian company, yet there’s been a lot of talk about the Section 232 petition here in the United States.

What's your take on Section 232 and the US Nuclear Fuel Working Group, and what effect its recommendations could have on Canadian uranium companies such as Skyharbour?

JT: Well, Mike, it has been a bit of a mixed bag, thus far, to be honest. Just to recap, you had the Section 232 petition back in 2018 and 2019 in which American uranium companies were pushing for an investigation into the worrisome supply situation in the US in which over 95% of uranium was imported for America’s nuclear fleet responsible for powering 20% of the country. To alleviate this potential national security issue, these producers were proposing that US nuclear utilities be required to buy 25% of their requirements from domestic sources of uranium.

The reality of that is, at current U3O8 prices, no uranium company in the United States can produce profitably so this quota, which was ultimately rejected by the White House in July 2019, would have brought on 10 to 12 million pounds of subsidized US supply.

So it was a positive for the sector as a whole as it prevented additional supply from coming online but an unintended consequence of Section 232 and the subsequently formed US Nuclear Fuel Working Group was that some US nuclear utility companies stuck to the sidelines refusing to enter into new longer term contracts to purchase uranium.

These utilities have been waiting for some clarity on where they're going to have to buy from and what their purchasing strategy should be going forward. Keep in mind that the US – the largest consumer of uranium globally – is now having to import close to 100% of its demand requirements.

Recently, nevertheless, we have seen some clarity from the US Nuclear Fuel Working Group with the announcement of a proposed 10-year, $1.5 billion uranium reserve budget. And Congress has now funded it.

As mentioned, a big chunk of uranium imports to the US are currently coming from Kazakhstan, Uzbekistan, and Russia, three nations that the Section 232 petition deemed to be adversarial and state-sponsored production centers. Just in the last few months as the DOC amended and expanded the Russian Suspension Agreement (RSA) to limit and reduce uranium imports from Russia through 2040 - up to 75% compared to the previous RSA. This is a positive development for any uranium company that has had to compete with Russian imports of uranium into the US over the last several decades.

The bottom line is having some resolution to the Section 232 and Nuclear Fuel Working Group as well as extending the RSA, there is a cloud of uncertainty in the US nuclear industry that has been lifted. It will allow US nuclear utilities to come back to the market, to start buying, and to start reentering long term contracts. However, the US does not have the production capacity to meet even a fraction of its annual requirements and it would take years to ramp up production. It is clear that the seeds the Trump administration have sown could really benefit Canadian uranium companies as bountiful, reliable, secure sources of uranium right across the border.

MF: It’s interesting because, as we’re seeing, the uranium spot price is beginning to move up, yet a lot of these junior uranium companies are still trading at low valuations.

Looking at Skyharbour Resources, what can you say about the company from a value proposition? And also, what's the long-term strategy… are you open to talks with a larger company in a buyout scenario?

JT: That’s an excellent question, Mike, and I think it serves as a good summary for our discussion. To me, the present value proposition for Skyharbour is the strongest it has ever been.

You can see that I've been purchasing quite a bit of Skyharbour stock over the last year. I've increased my position by buying in the open market and also by participating in recent financings. Several strategic investors have also come in with larger orders on these recent financings — institutional investors and family offices.

They see the value proposition of Skyharbour Resources as well.

Simply put, with a current market cap of only about C$27 million, and with the upcoming catalysts and news flow we have, I think it offers investors a compelling opportunity to gain exposure to the uranium market as well as high-grade discovery potential in the Athabasca Basin.

As noted, we have several active projects; a total of about 5,000 meters was just completed between us and our partner companies. We are also fully funded for additional drill programs this year at our flagship Moore Project, which will provide steady news flow through 2021. Furthermore, Orano just carried out a geophysical program to be followed up by a drill program.

There’s solid potential for new high-grade discoveries to be made as we continue to drill test our projects and in particular we are excited about testing the basement rocks at Moore. That’s where most of the recent high-grade discoveries have been made in the Athabasca and I think that approach gives us our best shot at emulating recent success stories and discoveries like NexGen, Fission, and Hathor.

So lots of company specific newsflow from our flagship Moore Uranium Project and as well from our partner companies Orano and Azincourt.

We also discussed our prospect generator strategy and our recent staking and land acquisitions. We’re looking to bring in other partner companies that can advance these projects, to provide additional news flow, and also to provide cash for Skyharbour.

We have recently added to our team and board of directors with the addition of Joseph Gallucci. Joe is a capital markets executive with over 15 years of experience in investment banking and equity research focused on mining and is currently the Managing Director and the Head of Mining Investment Banking at Laurentian Bank Securities Inc. His career has spanned across various firms including BMO Capital Markets, GMP Securities, Dundee Securities, and he was a founding principal of VIII Capital where he led the Mining Investment Banking Team.

Lastly, I think the uranium market timing is excellent. We’re seeing a rise in U3O8 prices, and hopefully that will continue through 2021.

You also have to keep in mind that Skyharbour is one of the few remaining active uranium exploration and development companies in all of North America.

It's one of the few go-to names if you want exposure to high-grade discovery potential, exposure to strategic partnerships with Denison Mines and Orano, exposure to a team with valuable M&A experience that’s made multiple high-grade uranium discoveries in the past.

So we're out there looking to make high-grade discoveries and delineate resources in the basin both with our own money and with partner-funded programs.

Ultimately, we'd like to be acquired by a larger company that can go in and develop the projects, which is what is what we did previously with Bayfield Ventures.

We are setting out to advance and value-add the project base, realize share-price appreciation and shareholder value creation along the way with the ultimate exit strategy of being bought out by a larger uranium company in a rising uranium market.

Furthermore, there aren’t many ways for investors to gain exposure directly to uranium as there are less than 40 pure-play, public uranium mining companies and a limited number of uranium centric funds, ETFs and physical holding companies. That means investment capital will work its way down to the small cap uranium mining companies quickly.

Those are some of the reasons why I believe the SYH value proposition is stronger than ever.

MF: Jordan, thank you again for taking the time. We’ll be closely following your company’s developments, as well as the uranium price, over the coming weeks and months.

JT: My pleasure, Mike. Stay well out there.

Why Uranium, Why Now?

The Athabasca Basin region, which plays host to Skyharbour’s flagship Moore Uranium Project, is known as the world’s leading source of high-grade uranium.

This massive geologic formation has been responsible for about 20% of the world’s uranium supply in recent years.

The United States is by far the world’s largest user of nuclear power with one-in-five American homes relying on nuclear generated power for electricity.

A full two-thirds of America’s clean energy consumption is coming from this source. In fact, nuclear is currently the world’s #1 source of clean energy… bigger than solar, wind, and all other renewable energy sources combined.

Our planet will continue to require clean nuclear energy as a means of mitigating the global warming effects of greenhouse gas emissions from coal and other carbon-based fuels.

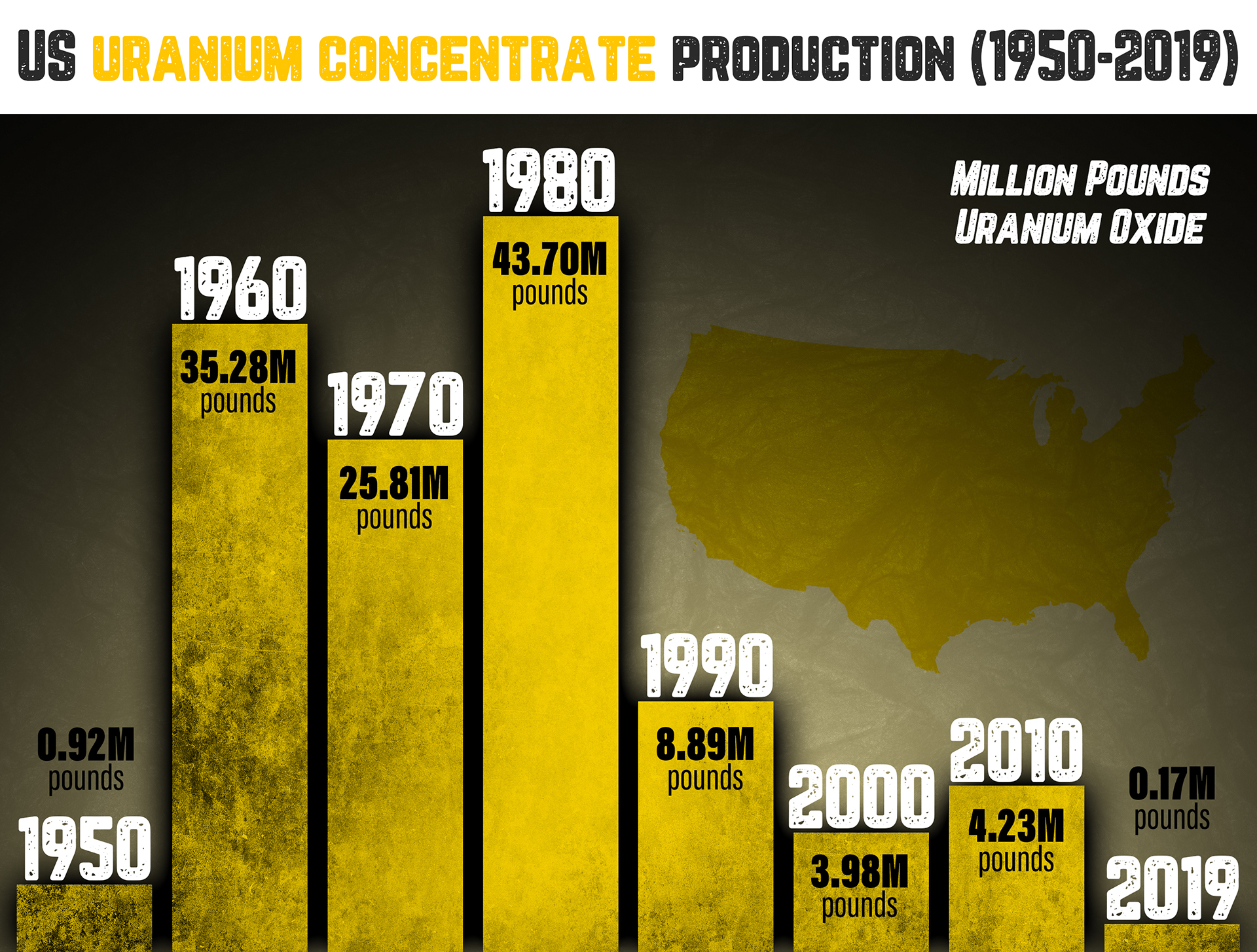

Yet, quite alarmingly, America is almost entirely dependent on foreign imports of uranium. That lies in stark contrast to the early-1980’s when our nation’s uranium was 100% Made-in-America.

Today, with crucial trade barriers removed, less than 10% of our uranium is derived from American sources.

That’s all about to change...

America consumes a staggering 50 million pounds of uranium every year. Yet, it produces under 0.5 million pounds… less than what it brought to surface back in the early 1950’s.

The US has 95 nuclear reactors… yet only produces enough fuel for one!

It should come as little surprise then, that in order to meet its robust demand, America imports a stunning 48 million pounds every year — making it over 90% reliant on foreign uranium sources.

And just WHO are some of America’s biggest suppliers?

Russia, of course, and its satellite states of Kazakhstan and Uzbekistan. In total, these nations supply around 40% of America’s U3O8 needs.

The risk to America’s national security is clear; drastic change is long overdue. That’s why the long-awaited recommendations from the US Nuclear Fuel Working Group in relation to the Section 232 Petition are so important.

With the creation of a US national uranium reserve and rising prices, we can reasonably expect US utilities to resume large-scale uranium market purchases, particularly as current term contracts with US producers draw to a close.

Plus, the threat of cascading indefinite mine closures and tightening supply as a result of the coronavirus pandemic has already begun to push uranium prices higher to above $30/lb today.

Scotiabank Global Banking and Markets said in a note that closing the Cigar Lake mine longer than the initial four-week period "has the potential to become the turning point in a ~10-year bear market."

It stresses that the site represents a "massive 13%" of global mine supply and 10% of total supply including secondary material.

Demand for uranium will keep rising…

Currently, there are 55 nuclear reactors under construction globally — most notably in China, India, and the UAE.

China has 47 nuclear reactors in operation — 12 being built now and many more slated to commence construction soon. Saudi Arabia has agreements to build 16 new reactors by 2040. Thus, you can see demand growth coming from all corners of the globe.

While it’s difficult to predict with any kind of certainty exactly WHEN uranium prices will catch up to global demand growth… the bottom line is that it WILL happen.

When it does, companies with world-class assets in safe mining jurisdictions like Skyharbour Resources should be among the first to capture disproportionate gains.

Keep in mind also that only 2 km of the total 4 km long Maverick corridor at Skyharbour’s flagship Moore Uranium Property has been systematically drill-tested.

That means there is robust discovery potential along strike and at-depth in the underlying basement rocks, which have seen limited drill testing historically.

Translation: There’s a lot of room for discovery and resource expansion by way of the drill.

In Closing...

Today’s uranium market is showing very compelling supply-demand fundamentals that should lead to an upward trajectory in the spot price for uranium.

We’re already seeing the beginning stages of this pending resurgence with the recent move from $25/lb to above $33/lb.

In my opinion, Skyharbour’s Moore Uranium Project is one of the top high-grade uranium exploration projects in the world. It checks every box — including size, grade, geology, and jurisdiction.

Skyharbour clearly stands out as one of the most compelling opportunities in the uranium exploration sector for speculators with the right time horizon.

I think the market will eventually wake up to the potential here… and any further upward movement in the uranium spot price could prove to be a powerful catalyst for higher share values.

For investors who are interested in the uranium market, now is an opportune time to take a close look at Skyharbour. Skyharbour Resources Ltd. trades on the TSX Venture Exchange under the symbol SYH and on the US-OTCQB market under the symbol SYHBF.

Yours In Profits,

Mike Fagan, Editor

Resource Stock Digest

Learn more about Skyharbour Resources and sign up to its investor list by CLICKING HERE.

CLICK HERE FOR THE MOST RECENT INVESTOR PRESENTATION.